May 05, 2022.

Way back, in 1944, at what is known as the Bretton Woods Conference, representatives of the nations of the world took the curious decision to designate the US dollar, which is actually a national currency, as the international currency. The rest, as they say, is history. In other words, the nations of the world in their collective wisdom decided to fix a square peg in a round hole and the world has been paying the price for this costly mistake ever since.

The concept of a national international currency is an unresolvable contradiction in terms that guarantees a conflict of interest. Something cannot be simultaneously black as well as white at the same time. Likewise, a currency cannot be simultaneously national as well as international at the same time. Or, maybe it can, but not without undesirable side effects.

Side Effects

The US dollar is a national currency because it is the monetary unit of the United States of America. It is therefore administered by the central bank of the United States, i.e., the Federal Reserve Bank, using monetary policies that are suitable to treat the fevers and chills of the US economy for the benefit of US citizens. However, when the rest of the world accepts the US dollar as the international currency, the rest of the world concomitantly accepts Federal Reserve Bank monetary policy as the world’s monetary policy although that policy was in fact designed for the US economy and may represent a conflict of interest between the US economy and the world economy.

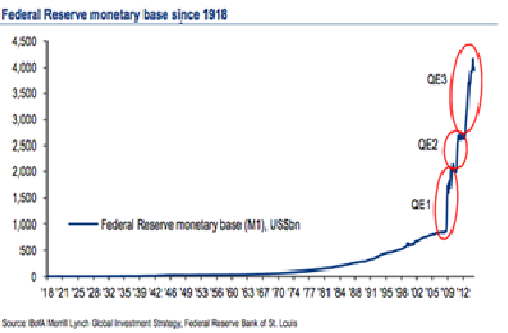

The Federal Reserve Bank has a mandate to manage monetary policy to control inflation and employment within the borders of the United States alone. As such, the Federal Reserve Bank is only secondarily interested in the fevers and chills of the global economy. Indeed when the Federal Reserve Bank administers an injection of monetary stimulus, which may be what the doctor ordered as treatment for a chill in the US economy, it usually ends up creating a fever as the inevitable side effect in the world economy. Remember the old saying – when the US sneezes the world catches cold.

This conflict of interest between the Federal Reserve Bank’s national priorities and international secondary priorities may not matter all that much when the fevers and chills of the US economy are relatively mild. But when those US fevers and chills reach the stupendous proportions of the Subprime Mortgage Crisis or the Coronavirus Crisis the resulting consequences for the global economy become difficult to ignore.

Guns and Butter

One of the intractable problems with a national international currency is that the nation issuing that currency is forced to maintain a permanent balance of payments deficit with the rest of the world. The system simply will not work without such a deficit since it would otherwise cause a lack of international liquidity without which international trade will be impossible. It also means that that United States deficit is funded by the rest of the world.

As a result, the US government has plentiful supplies of money since its deficits are funded by the rest of the world. After all, money is meant for spending and these deficits have enabled the US government to survive the subprime crisis, set up large numbers of military bases all over the world, run the world’s largest navy with eleven aircraft carriers, engage in serial military misadventures all over the world and fancy itself as a global policeman willing to browbeat errant nations into submission at the slightest pretext.

These plentiful supplies of money funded by the rest of the world have ensured that the United States does not have to make the classical choice between guns and butter – they could tote their guns and slurp their butter at the same time. In the meanwhile, the rest of the world is in a perpetual scramble to export anything and everything to the United States so that they can earn US dollars and build up their US dollar piggy banks in order to have some international spending money. Many nations even go to the extent of deliberately undervaluing their currencies with reference to the US dollar to gain a competitive advantage so that their exports are cheaper for US citizens – China, arguably rose as a result of such competitive undervaluation of the Yuan.

These US deficits widened even further after the Asian Currency Crisis in 1997 when nations all over the world swore never to suffer the same fate ever again. The silver bullet to solve the problem was for the rest of the world to amass bloated reserves in the international currency in order to accumulate enough reserves as firepower to stave off any attack on the domestic currency in foreign exchange markets. This led to a burgeoning US external deficit and a US banking system that was inundated with cash which ultimately led to the Subprime Mortgage Crisis in the United States in 2008.

Money for Nothing, Cheques for Free

These days the US economy seems to stumble from one economic crisis to the next and then bails itself out by pumping up its deficit with wild abandon fuelled by the recklessness that only free money can bring. The US government can pump up the deficit at will knowing that the rest of the world will have no choice but to pay for that deficit.

The Coronavirus struck at the heart of every economy and prompting all governments to provide some kind of relief to their citizens. But the US government pulled out all the stops by deficit financing programs that supported debt markets, protected payrolls, propped up failing businesses, etc. US citizen’s payrolls were protected whereas by contrast migrant workers in India had to find their way back to their native villages on foot.

Monetary Policy Export

It is a well understood fact that a national international dollar causes the export of US monetary policy to the rest of the world.

For example, imagine a situation where the Federal Reserve Bank loosened monetary policy, i.e., reduced interest rates and increased money supply, to stimulate the US economy in response to a US recession. A loose monetary policy fuels inflation and since the US dollar is the international reserve currency, it means that it fuels inflation internationally in all internationally traded products including such commodities as crude oil, base metals, etc. which are vital inputs to global industry. This cost push inflation forces the rest of the world’s central banks to tighten monetary policy in response to the Federal Reserve Bank’s loose monetary policy thus throttling their own economies. In other words, the rest of the world has to suffer a recession to facilitate a US stimulus.

The world’s poor, like the poor migrant workers in India who trudged to their native villages on foot at the height of the pandemic will ultimately pay for a US stimulus that protected US payrolls during the pandemic. It’s time to call a halt to the Bretton Woods madness.