Abstract

Stock markets of emerging economies of Latin America and Asia Pacific region play an important role in a global portfolio as these markets promise better risk-return profile to investors.

Hence it is of interest to international investors to analyze the pattern and causes of comovement between these emerging equity markets with developed market like the USA.

The findings suggest that Latin American emerging equity markets share a higher degree of comovement with USA as compared to its counterparts in Asia Pacific region.

Further, the 2008 global financial crisis had a deep impact on stock market comovement between Latin American markets and USA.

The Asia Pacific emerging markets were able to withstand the effects of crisis.

The results indicate bilateral trade relationship and distance as the key determinant that influence stock market comovement between emerging markets of both the regions and USA.

Keywords: Emerging Markets, Latin America, Asia Pacific, Stock Market Comovement, DCC GARCH

Introduction

International investors are always in search for attractive investment avenues that can improve the diversification benefits of their portfolio.

Emerging markets of Latin America and Asia Pacific regions are gaining prominent mindshare among global investors.

Latin American equity markets showed signs of recovery after 2015 resulting in increased investor confidence.

Asia Pacific region remains one of the fastest growing regions globally and continues to attract investors because of strong macroeconomic fundamentals.

The study examines:

- The degree of stock market comovement between emerging markets and USA

- The impact of the 2008 global financial crisis

- The determinants influencing stock market comovement

Literature Review

Stock market integration has significant implications for international diversification and capital allocation.

Several studies reveal strong relationships between emerging and developed markets.

Research highlights trade relationship, financial integration, GDP growth differentials, inflation, and political crises as major determinants of stock market comovement.

The present study contributes by comparatively analyzing Latin America and Asia Pacific regions.

Data and Research Method

The study includes emerging markets of Latin America and Asia Pacific.

Latin America markets include:

- Brazil (IBOVESPA)

- Chile (IPSA)

- Colombia (COLCAP)

- Mexico (S&P/BMV IPC)

- Peru (S&P/BVL PEN)

Asia Pacific markets include:

- China (SSE Composite Index)

- India (Nifty 50)

- Indonesia (JCI)

- Malaysia (KLCI)

- Philippines (PSEi)

S&P 500 represents USA market.

Data spans from 1 January 2002 to 31 December 2017.

DCC-GARCH Method

Dynamic Conditional Correlation Generalised Autoregressive Conditional Heteroscedastic (DCC GARCH) model developed by Engle (2002) is used.

Daily stock returns are computed using logarithmic differences of stock prices.

Bai and Perron structural break test is employed to examine the effect of the 2008 global financial crisis.

Structural Break Test

Bai and Perron’s multiple structural break test is used to analyse crisis spillovers during the 2008 global financial crisis.

Structural breaks mainly occurred during:

- 2008–2009 Global Financial Crisis

- 2012–2013 Quantitative Easing period

- 2015 Flash Crises

Pooled Regression

Pooled Ordinary Least Squares regression with clustered standard errors is employed to identify determinants of stock market comovement.

Variables considered include:

- Bilateral trade relationship

- GDP growth differential

- Inflation differential

- Market capitalization

- Stock turnover ratio

- Global Financial Crisis

- Distance

Results

Preliminary Analysis

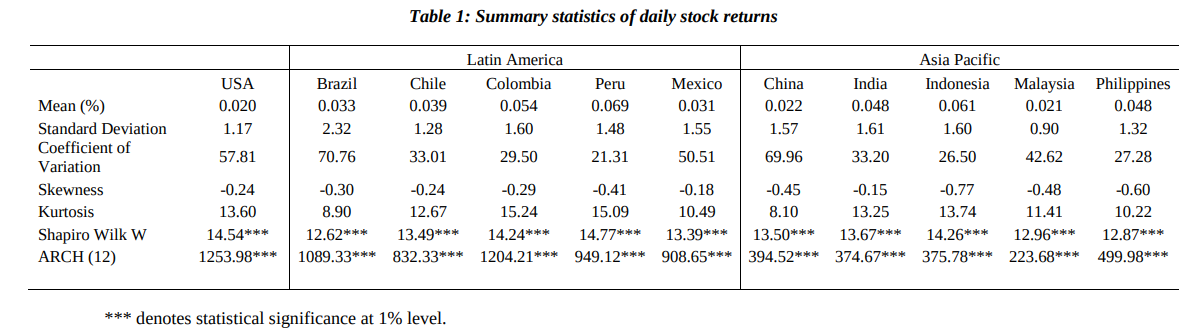

The descriptive statistics show that Peru, Colombia, and Chile are top performers in Latin America.

Indonesia, India, and Philippines showed the highest returns in Asia Pacific.

Stock returns across both regions are negatively skewed and leptokurtic.

Table 1: Summary statistics of daily stock returns

Dynamic Conditional Correlation GARCH

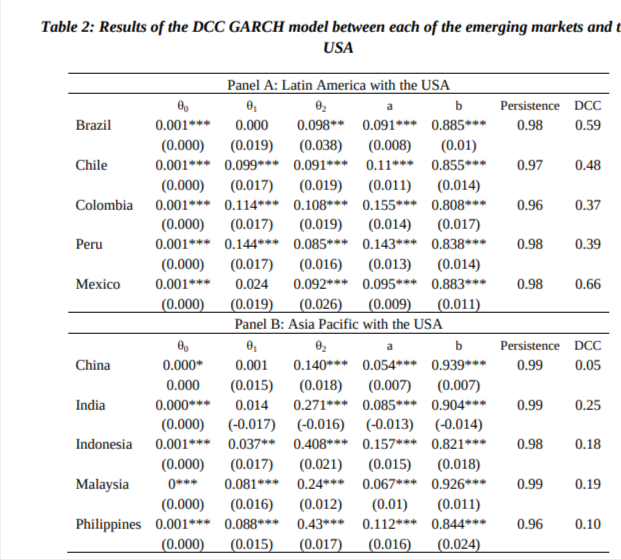

Results reveal that USA significantly influences emerging markets across both regions.

Latin American equity markets show stronger comovement with USA compared to Asia Pacific markets.

Asia Pacific markets offer better diversification benefits to global investors.

Table 2: Results of the DCC GARCH model between emerging markets and USA

Structural Break Analysis

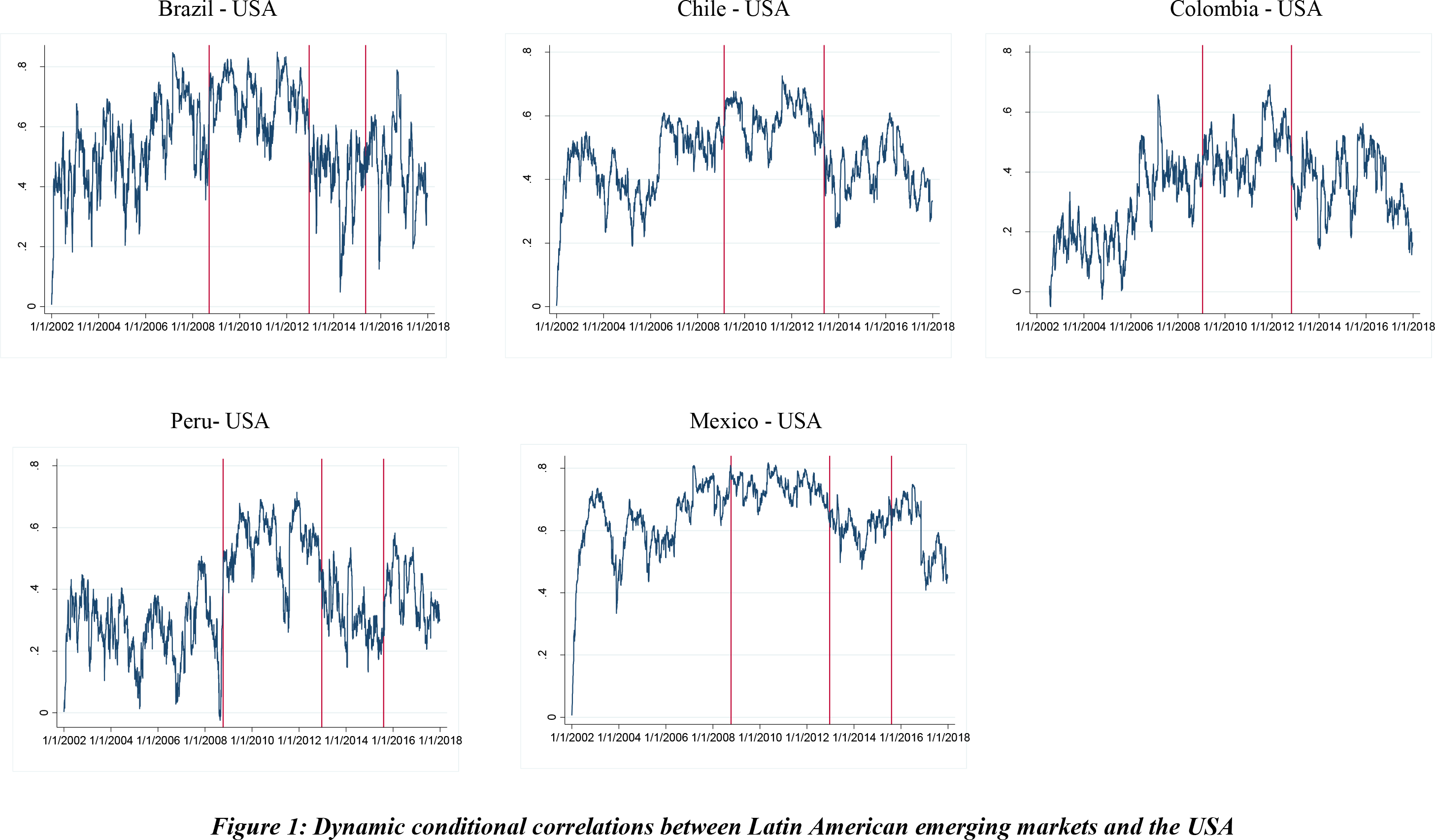

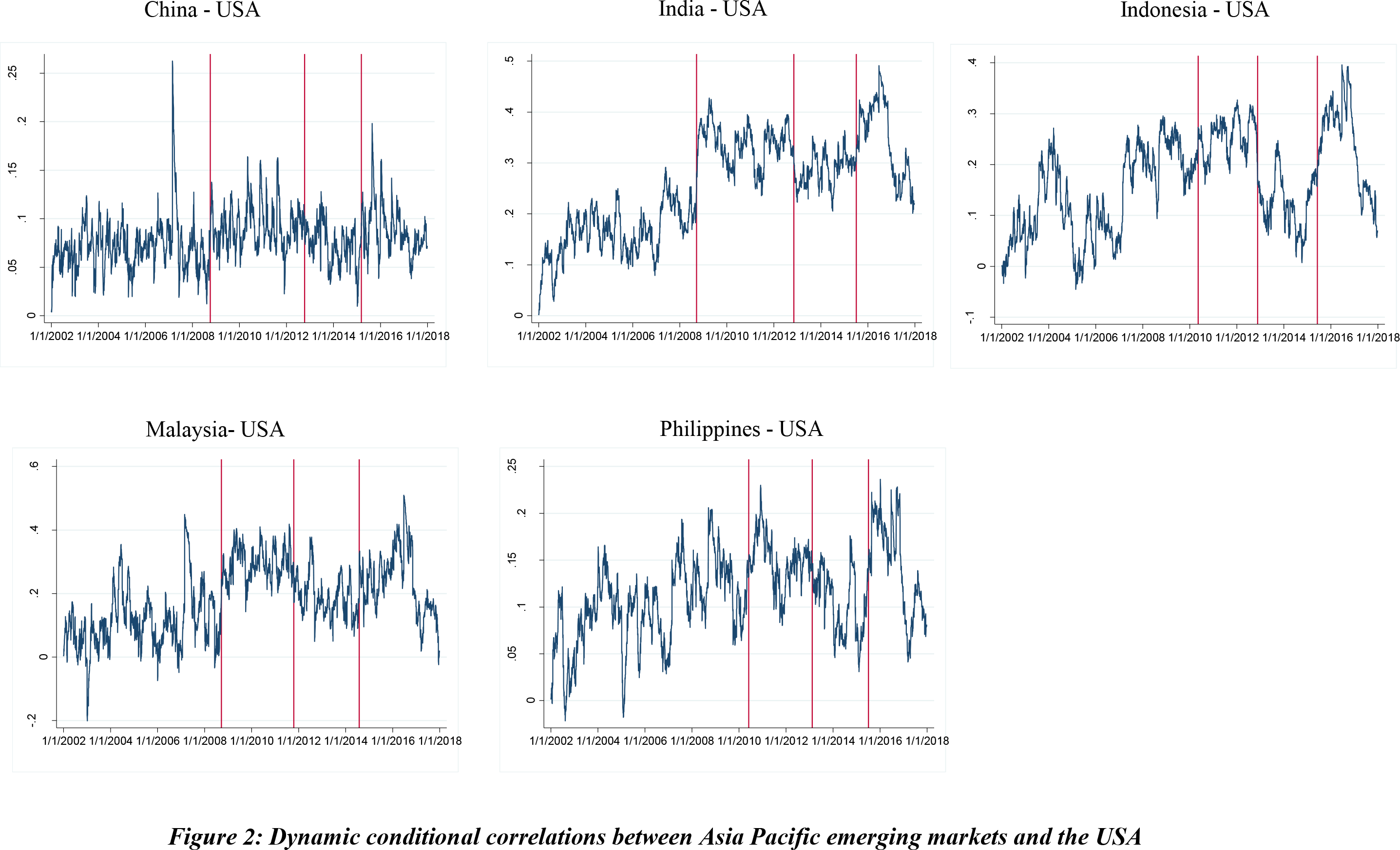

Structural breaks identified by Bai and Perron test indicate that the 2008 financial crisis significantly affected stock market comovement globally.

Latin American markets exhibited contagion, herding, and post-crisis adjustment phases.

Asia Pacific markets were comparatively resilient during the crisis.

Figure 1: Dynamic conditional correlations between Latin American emerging markets and the USA

Figure 2: Dynamic conditional correlations between Asia Pacific emerging markets and the USA

Pooled Regression Results

Bilateral trade relationship, distance, and global financial crisis are major determinants influencing stock market comovement.

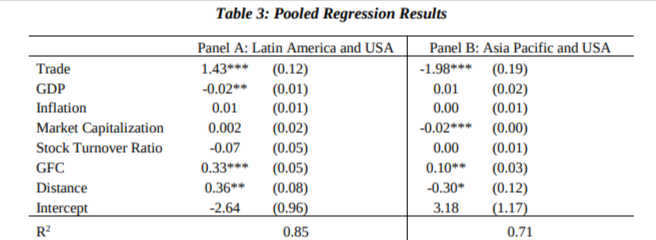

Trade relationship positively influences Latin American market integration with USA.

Market capitalization differential significantly impacts Asia Pacific market comovement with USA.

Table 3: Pooled Regression Results

Conclusion

The study confirms that USA acts as a major global disturbance factor influencing emerging equity markets.

Latin American markets are more strongly integrated with USA compared to Asia Pacific markets.

Asia Pacific emerging markets provide better diversification opportunities to investors.

The 2008 global financial crisis had a deeper effect on Latin American markets than Asia Pacific markets.

Bilateral trade relationship, distance, and global financial crisis are significant determinants of stock market comovement.

References

Alotaibi, Abdullah R, and Anil V. Mishra. “Time varying international financial integration for GCC stock markets.”

Arouri, Mohamed El Hedi, Mondher Bellalah, and Duc Khuong Nguyen.

Bai, J, and P Perron. “Computation and analysis of multiple structural change models.”

Batareddy, Murali, Arun Kumar Gopalaswamy, and Chia-Hsing Huang.

Cardona, Laura, Marcela Gutiérrez, and Diego A. Agudelo.

Chen, Mei-Ping, Pei-Fen Chen, and Chien-Chiang Lee.

Chiang, T. C, B. N Jeon, and H. Li.

Chuliá, Helena, Montserrat Guillén, and Jorge M. Uribe.

Engle, R. “Dynamic conditional correlation.”

Engle, Robert F. “Autoregressive Conditional Heteroscedasticity.”

Forbes, Kristin J., and Menzie D. Chinn.

Frijns, Bart, Alireza Tourani-Rad, and Ivan Indriawan.

Gilmore, C. G, and G. M. McManus.

Huyghebaert, N, and L Wang.

Johnson, Robert, and Luc Soenen.

Kim, Sei-Wan, Young-Min Kim, and Moon-Jung Choi.

Krugman, Paul. “Lessons of Massachusetts for EMU.”

Lee, Hyunchul, and Seung Mo Cho.

Lucey, B. M, and Q Zhang.

Mollah, Sabur, A.M.M. Shahiduzzaman Quoreshi, and Goran Zafirov.

Narayan, S, S Sriananthakumar, and S Z Islam.

Paramati, Sudharshan Reddy, Eduardo Roca, and Rakesh Gupta.

Pretorius, Elna.

Syriopoulos, T.

Voronkova, Svitlana.

Wälti, Sébastien.