LEAN ACCOUNTING: A Strategic Approach to Cost Management

Conventional accounting process – recording, classifying, summarizing business transactions – despite advances in technology – is a complex process, let alone the execution, even the understanding. The entire process is non-value adding and ends up to a wasteful expense.

Lean Accounting refers to the process of managerial accounting and control systems of an enterprise by applying lean methods. Lean methods are drawn from technological innovation called – “lean manufacturing” by Toyota and other Japanese companies in the 1980s. The objective of lean method is to eliminate waste, free up capacity, speed up processes, defect-free, clear and understandable processes. It was in the mid of 2000s that a Lean Accounting Summit was organised in Detroit to propose Principles, Practices and Tools of Lean Accounting.

The objective of this article is to discuss in brief few selected approaches of lean accounting to highlight the benefits of the same:

Value Stream Costing

Value stream costing suggests the manufacturing company to create cost sheets on a weekly basis by

recording all the direct costs associated with the production and sale. For instance, every time a value stream. Every time a payment towards wage is made, it enters into value stream, irrespective, whether it’s direct or indirect. Overheads need not be allocated at all, if such process is going to take higher efforts. The weekly summarising ensures a continuous control and also quicker understanding by anyone. (Baggaley, 2003)

Figure 1: Example of Value Stream Costing

Plain English Financial Statements

Financial Statements must be such that they are understandable by anyone in the company. This ensures minimization of errors in financial statements, misleading window-dressing and allows for meaningful analysis for decision-makers.

Hoshin Policy Deployment

Contrasting the long-term business strategy planning, Hoshin policies are strategic statements which clearly state plan of action for the next year. Be it the resource planning, marketing targ

ets or cost standards at all levels of management. Another differentiator of Hoshin policy is that it develops plans that need to be executed by the plan-makers themselves, rather than the subordinates. (Maskell & Baggaley, 2006)

Target Costing

A cost control mechanism successfully demonstrated by Sony’s Walkman case, target costing suggests to set the target market share that the company wants to acquire, and work in the reverse order to arrive at the maximum cost within which the product needs to be produced and sold. Tata Motors Nano is case for this point.

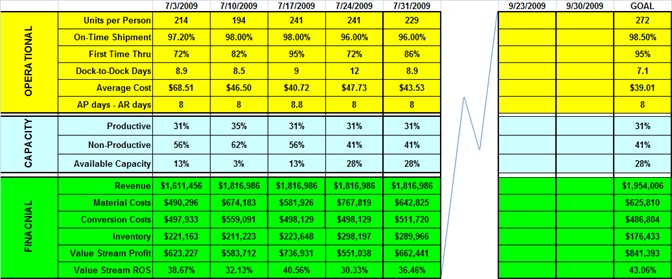

Box Score

Box Score acts as a daily/weekly scorecard to display for the information of one and all connected to the production process and adjust the velocity of efforts to match the pace required to march towards the set short-term goals. A typical box score card would contain operational, capacity, and financial goals and easily conveys the distance to cover. (Lean Accounting, n.d.)

Figure 2: Example of Box Score Reporting

Backflush Costing

Generally used with JIT systems, this approach suggests eliminating the regular cost tracking systems, instead carry out the costing process after the production run. Costs are ‘flushed back’ to cost units using real data. This eliminates the cost of work-in-process and simplifies the costing system.

Above-discussed are only few of the operational strategies that (mostly manufacturing) firms can install into their processes and are bound to yield results. Having said the same, it must also be noted that there are certain challenges that a firm that adopts a lean accounting needs to face – (i) Is this going have its impact on matching compliance requirements – like the accounting standards; (ii) What would be the cost of transforming into the new system and how long does it might take to see the payback? (iii) What would be the potential reactions from different stakeholders?

Despite its limitations and challenges, lean accounting charters continue to be desirable. Organisations across, (specially the advanced economies) have been consistently adopting and at the same time innovating lean accounting practices, in parts, at least.

Works Cited

2015 Lean Accounting Summit & Lean Management Summit. (n.d.). Retrieved 12 4, 2015, from http://leanaccountingsummit.com/

Baggaley, B. L. (2003, May/June). Costing by value Stream. Journal of Cost Management, 17(3), 24-30. Retrieved 12 4, 2015, from http://www.maskell.com/lean_accounting/subpages/lean_accounting/costing_by_value_stream.html

Lean Accounting. (n.d.). Retrieved 12 4, 2015, from Wikipedia The Free Encyclopedia: https://en.wikipedia.org/wiki/Lean_accounting

Maskell, B. H., & Baggaley, B. L. (2006). Lean Accounting: What’s It All About? Target Magazine.

payment towards purchase of materials is made, it is recorded in the