This version is dedicated to the concept of YTM or Yield to maturity. If somebody buys a bond when a Bond is launched i.e. 11% ITC 2024, he will buy it at 100/- per bond. Now as time progresses, that bond is available for secondary sell too. It is like an apartment is sold at 70Lacs when sold new, but as time progresses it could be resold at 85 Lacs also or 67 Lacs also depending on demand and supply and could be many more important deciding points. That is called market pricing. In bond the market price is determined by inflation. If inflation increases more discounting happens and bond is available at a cheaper price, if inflation moderates less discounting happens and prices go up, so bond is available at a considerable higher price.Yield to Maturity (YTM) refers to the required rate of return a bondholder will expect to receive provided they hold it all the way till maturity (called as Hold till Maturity).While reinvesting all coupon payments at the bond yield. It should not be confused with holding period return, as the two often differ. Interesting case will happen for zero coupon Bonds though; in this case the YTM will always equal the Coupon rates the only payment happens at the end or at maturity.[1]Sharia Bonds will have the similar fate as far as YTM is concerned. So, while buying Sharia Bonds or any other deep discount Bonds, YTM becomes of no use.

Another way of putting it is that the yield to maturity is the rate of return that makes the present value (PV) of the cash flow generated by the bond equal to the price. Yield to maturity is widely used by investors as a way to compare bonds with different face values, coupon payments, and time till maturity.

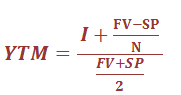

Situation 1

9% GOI 2024 with a credit rating of AAA (So) is available at 93/- per Bond in secondary market after 1 year of issue

Face Value is 100 (=FV)

Selling Price is 93 (=SP)

Left over years are 9 (=N)

Coupon is 9 (=I)

So, if an investor buys at 93, actual gain is 10.13% and not 9%. So, YTM is 10.13%.

Situation 2

9% GOI 2024 with a credit rating of AAA (So) is available at 105/- per Bond in secondary market after 1 year of issue

Face Value is 100 (=FV)

Selling Price is 105 (=SP)

Left over years are 9 (=N)

Coupon is 9 (=I)

Once a bond has been issued and it’s trading in the bond market, all of its future payouts are determined, and the only thing that varies is its market ask price. The buying zone however depends on the YTM, if the YTM is high; the Bond will be available at a discounted price, also when the YTM will be considerably lower than the coupon the Bond will be available at a significantly higher price.[2]This buying zone and selling zone links the connection between YTM and Inflation, or in other words “Required Rate of Return”. That means that’s the minimum return to offset the adverse effect of inflation.

The yield to average life calculates the yield using the average life of a sinking bond issue. So for a 10-year bond with anotification that specifies that 10% of an issue must be retired each year from the 5th year to the 10th year of the bond’s term, the average life would be 5 years, provided the convexity is not under consideration.

The yield to average life is also used for asset-backed securities, especially mortgage-backed securities, because their lifetime depends on prepayment speeds of the underlying asset pool.[3]

Yield to maturity is the average yield over the term of the bond.If a bond is sold before maturity, then its actual yield will generally be different from the yield to maturity. If interest rates rise during the holding period, then the bond’s sale price will be less than the purchase price, decreasing the yield, and if interest rates decrease, then the bond’s repurchase price will be greater. The holding-period return is the actual yield earned during the holding period. It can be calculated using the same formula for yield to maturity, but the sale price would be substituted for the par value, and the term would equal the actual holding period. Note that, unlike yield to maturity, the holding-period return cannot be known ahead of time because the sale price of the bond cannot be known before the sale, although it could be estimated.Money market instruments are short-term discount instruments with maturities of less than a year and they are having mark to market link too, so the interest is paid at maturity. Because short-term instruments are issued at a discount, their yield is often referred to as a discount yield, which is often annualized as the bond equivalent yield (BEY) which simplifies the comparison of yields with other financial returns.

It is important to note that callable bonds should receive special consideration when it comes to YTM. [4]Call provisions limit a bond’s potential capital gain because when interest rates fall, the bond’s price will be limited up to the celling of their respective Call price. Thus, a callable bond’s correct yield, called the yield to call, at any given price is usually lower than its yield to maturity. As a result of this, investors generallyconsider the lower of the yield to call and the yield to maturity as the more tangible indication of the return on a callable bond.

In the abovementioned CCIL real time rolling settlement screen the LTY (last Traded Yield or YTM) is 7.7%, whereas the security is offering a coupon of 8.40%, the premium in the bond i.e. the availability is at 104.45 instead of 100, has lowered the YTM.

References