Demystifying Bonds- an exploratory work

By

Bikramaditya Ghosh, Asst. Prof.

This small attempt is to demystify the Accrual & Duration strategies of Bonds along with Duration Concept for Bonds. These are generally used for Treasury & Cash Management activities by Banks & Corporates of decent size. Generally the common notion is that, Bonds are to be invested for a periodic cash flow back, for a fixed period. The Cash flow too is fixed, so they are called Fixed Income segment. So, the coupon rate on offer along with the credit rating are the two cardinal parameters to look out for. Credit Rating is another crucial factor for the selection of Bonds. The higher the Rating lower the coupon on offer, and the lower the rating higher the coupon on offer. A GMR 10 Year Bond with a BB+ rating may fetch as high as 14.5% compared to a TISCO 10 Year with AA+ will offer a 9.2% and a GOI of 10 Year will offer 8.17% at the same time. However we will not discuss that issue in this version.

So the Bond in consideration here is 8%GS2024. That means 8% is the annual coupon, the Bond belongs to Government of India (Sovereign Security) & the tenure is 10 Years. When a new bond is issued by the issuer (in this case it is GOI) the coupon is set in and around the CPI prevailing at that time. This is done to take care of the purchasing power of the economy & its people. Otherwise the purchasing power parity will be lost, which in turn could be detrimental for a consumption led economy such as India.

If an investor buys the bond at the issue time and hold it till maturity, he will be assured to get 8% (important to note that CPI is also at 8% at that time), that method is called hold to maturity (HTM) or Accrual.

If a new investor looks at the bond when CPI is 8.13%, so he will buy the same bond at 991 (9 rupees discount), which means as CPI has been more than the Coupon Rate the Selling Price of the Bond goes below the Face Value, assigned when it was launched. This in simple term means for 1 unit of the Bond the investor has to pay 991 instead of 1000. So, his effective Yield will be 8.07% and not 8%. So, he will gain marginally.

Similarly when CPI is at 7.92%, that is lower than the CPI figure, when the Bond was issued (i.e. 8%) the Selling Price of the Bond becomes 1006. So, anybody who wants to buy the bond later at that time have to pay 6 rupees premium. This in simple term means for 1 unit of the Bond the investor has to pay 1006 instead of 1000. So, an intelligent investor will buy the bond when it is at 991 & subsequently sell it when it is 1006, thus making a Capital Gain of 15 on 991, so, making an additional 1.51% Capital Gain in a short while.

This is how Bond trading happens in the short term. Interesting to note here, that when he is buying the bond the CPI is at 8.13% and at the point of selling the bond the CPI is at 7.92%. So, in Bonds we say, when inflation is higher than your Coupon, you buy, and when inflation is lower than your Coupon you sell. This Strategy is called Duration.

Buying Zone | Selling Zone | ||

CPI | 8.13% | CPI | 7.92% |

Price | 991 | Price | 1006 |

This takes us into one more interesting but complex calculation, called Duration. Let us take an easy example to understand. If two trucks are going at the same speed, one with huge luggage, and another without any luggage, then the propensity to topple will be higher for the heavy truck (with luggage). A physicist will be referring to the concept of “Center of Gravity” and will confirm that the higher the Center of Gravity the higher the instability. Duration is similar, the higher the Duration the more the Risk. Here Risk means Price fluctuation Risk for that Bond.

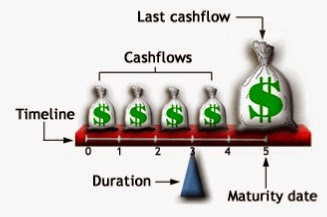

A [i]measure of the sensitivity of the price (the value of principal) of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years. Rising interest rates mean falling bond prices, while declining interest rates mean rising bond prices. The image below mentions it nicely. So, it means that approximately half the Present Value is paid before the point of Duration, and half the present value is paid post the point of Duration. So, the shorter the Duration is the better it is from the perspective from Risk.[ii]Treasury judiciously uses Duration Strategy, for profit maximization, along with taking care of the duration in to account. Our next series will be based on Computation of YTM & Duration. So, in other words, Duration will act as a “Pivot” for the cash flow, scheduled for future days or Years to come.

[i] http://www.investopedia.com/terms/d/duration.asp