Sakeerthi S

The difficult times surmounting the Indian economy by now is a widely talked about topic. One fine day, while having a discussion with one of my ex-boss about this, the one question he put forward in front of me made me dwell on the deeper aspects of this grave situation. He asked me, being a finance person what do you think the current status of our economy is, Is it undergoing a recession or running into that stage? With my limited knowledge of reading newspapers and articles about this, I could say that it’s not a recession, but its a “Growth Recession” that is happening in the economy as of now. But when he asked about the reason for this I was almost blank. Before going into the details, it’s necessary to have a glimpse of certain facts.

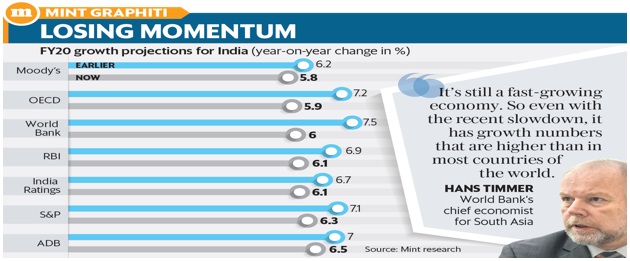

The World Bank has projected India’s growth rate to fall to 6% in 2019-20, which stood at 6.9% in 2018-19 and 7.2% in 2017-19. The World Bank report also noted that the current account deficit had widened to 2.1% of the GDP in 2018-19 from 1.8% last year, mostly representing a deteriorating trade balance. Even the latest annual report of the RBI for the financial year 2018-19 (FY19) confirmed that the Indian economy is going through one of its worst phases. The GDP growth rate for the economy has slipped to 5% in the first quarter of FY20, the lowest in over 6 years. Let’s have a look at Mint Graphiti which supports these figures.

Alarming, Right???

Be it the downturn of the automobile sector of the country, mounting NPA issues of the Indian Banks, sluggish consumer demand or collapsing manufacturing sector. Do all these indicate the crisis brewing the Indian economy?

A “recession” is defined in economics as three consecutive quarters of contraction in GDP. But “contraction” is a rarity in a large developing economy like India. Hence the current phase through which the country is going through can be defined as a “Growth Recession” rather than a “Recession”. The last reported negative growth of India was in 1979. A growth recession can be defined as a phenomenon where an economy grows but at a much slower pace than the usual one for a sustained period.

Causes for the present slowdown

According to the credit rating agencies across the globe, India was supposed to witness a booming phase from 2014 (the year in which the current government came to power) and the growth rates of 2014 and 2015 justified those predictions. But all of a sudden the situation reversed. A few major reasons that have caused this downturn could be:

· Reduced Consumption (inclusive of both private final consumption expenditure and government final consumption expenditure):

Over the past 5 years, the total consumption expenditure by the Indian households had accelerated with an average growth rate of 7.8% compared to an average of 6.1% in 2011-14. But the recent fall in PFCE in the June quarter to 3.1% compared to the 7.2% in March quarter has significantly contributed to the recent slowdown.

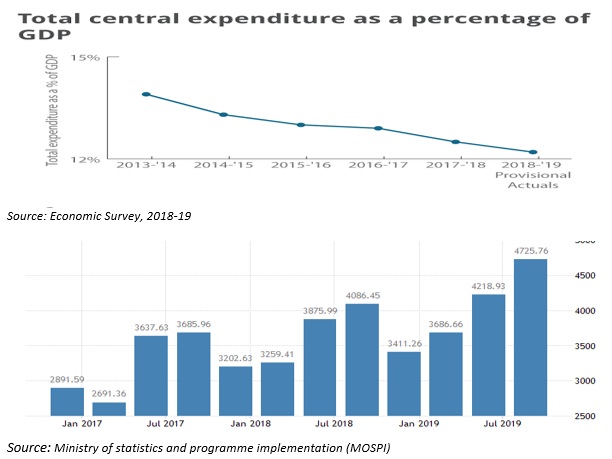

Investments or spending by the government:

Although GFCF (Gross Fixed Capital Formation), the main constituent for investment in an economy increased, yet its contribution to the growth fell by 6.2% of the GDP in 2014-19 than in 2011-14. Let’s have look at our government’s spending over the last three years:

· Demonetization:

Consumers developed a habit of hoarding cash in banks instead of spending or investing elsewhere as a result of demonetization. Rural India was hit worst in terms of demand as entire rural India runs on cash and demonetization has led to the squeezing of cash in circulation in such areas and caused a large number of job cuts. Since the cash crunch caused by demonetization has left SMEs dry, they also started withholding investments causing the economy to shrink.

· Mounting NPAs

India’s banking system has lost $24.8 billion due to NPAs of 416 defaulters being written off. The government has pumped in billions of dollars to help the debt-laden state lenders in exchange for them implementing the proposed banking reforms.

· Rollout of GST

Although it could prove to be good for the economy over the long run, for the time being, it has hampered the growth of the industry and agricultural sector, especially SMEs. And SMEs are now showing a tendency to withhold inventory until they migrate to the new GSTN or GST network completely and make themselves compliant to the new rules and regulations under it.

· Global slowdown

It’s not just India, but the whole globe is facing a growth stagnancy, which in some or the other way is impacting our economy as well because India is largely a net export-oriented country.

· Retreat of Globalization

Policies of the Trump administration have contributed to a decline in the number of students and professionals going to the US and to add on to it, the Brexit uncertainties have compounded the situation.

Where QE can play a vital role in dampening the growth recession?

The commercial bank lending rates have turned so much immune to the monetary policies that even a sixth reduction this year I the benchmark price of money is hardly making any difference. It’s recently that I came across a concept called QE (Quantitative Easing) widely followed by many countries including the US, which none in our economy is even speaking about. Looking at the various aspects of this and how successfully the US has implemented this, I think this to an extent can help our economy to revive from the current situation, although not repair the damage already done.

QE has got a couple of advantages. Firstly, it lowers the long-term government bond yield that reduces loan costs for risky borrowers since government bond yield act as a benchmark. Secondly, a more liquid banking system with more low yielding cash than high-yielding bonds will be impatient to lend- at least in theory. Yet, this type of QE relies a lot on loans being made or lending. If the demand from the borrower side is struggling the impact of this technique might be limited as it does not increase the money supply in the broader economy. But in the case of our economy, there is a probable solution for this sit

uation as well. In India, this will help RBI to buy government bonds from non-banks, following the model of the US Federal Reserve, which primarily purchases securities from hedge funds, broker-dealers, and insurance companies. Since non-bank sellers on bonds don’t have accounts with RBI, they will deposit any cash they receive with other commercial banks letting more money with such banks for lending, even without running behind deposits or demanding the cash pumping by RBI and will give way for the security deposit of RBI to be used for other purposes. Money supply will thus increase in the economy even without making new lending. This, in turn, will revive the economy over the coming years.

uation as well. In India, this will help RBI to buy government bonds from non-banks, following the model of the US Federal Reserve, which primarily purchases securities from hedge funds, broker-dealers, and insurance companies. Since non-bank sellers on bonds don’t have accounts with RBI, they will deposit any cash they receive with other commercial banks letting more money with such banks for lending, even without running behind deposits or demanding the cash pumping by RBI and will give way for the security deposit of RBI to be used for other purposes. Money supply will thus increase in the economy even without making new lending. This, in turn, will revive the economy over the coming years.

Conclusion:

From Moody’s 6.2% earlier growth projection to the current 5.8% prediction and World Bank’s 7.5% growth prediction to the current 6% growth prediction, India is feeling the heat of a growth stagnation. Although the government and the central bank is putting up all the best possible efforts to revive the economy out of this current phase, results are either slow or not visible at all. Although the various monetary policies of RBI and the fiscal policies of the government are directed towards achieving this objective, a phase has arrived where the impact of such operations are yielding little or no results. This is where the concept of QE could come to rescue. The method was widely accepted as the key factor which has pulled the US out of the 2008 recession. And the same could be implemented by RBI in India. But again there is a question about the success rates that could be assured with this phenomenon as the Bank of Japan had declared “QE as ineffective” in the case of Japan. How well RBI and the GoI can together overcome the negative aspects of this method and implement it successfully will determine the success rate. The challenge would be to ensure the growth rate would get have been worse without the implementation of QE. Also, since the money created through QE was used to buy government bonds from the financial markets, the newly created money directly goes to the financial markets, thereby spurring the prices of such assets, pushing up inflation and devaluing the currency over the time run. This would be a great challenge for a country like India which is highly sensitive to inflationary trends. A far more effective way to boost the economy would be to create money, grant it directly to the government and allow the government to spend it directly into the real economy, which will be more effective.

Sources:

Disclaimer: The views, opinions and content on this blog are solely those of the authors. ISME does not take responsibility of content which are plagiarized or not quoted