Kiran Kumar K V, Faculty-Finance & Analytics, ISME

On a random day (to be precise 08-August-2019), I was browsing through Economic Times and found some news items interesting and attempting to convey something about the overall outlook on market.

First, RBI cut the repo rates by 35 basis points, which came as an absolute surprise to the market. But, the reasons quoted, need more attention – estimated GDP growth rate was brought down to 6.9% from the earlier 7%, boost the NBFC liquidity through reduced interest rates, as well as through lowered risk weights to retail lending and raising bank exposure limits for NBFC.

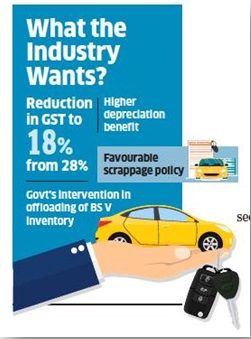

Second, Tata Steel Q1 net profits drop by 63%, while the company has called off its JV with a HBIS, its south east Asian subsidiary, broke its JV with ThyssenKrupp, European business partner and management openly stating, they’re trimming their capex plans, till economy revives.

Fourth, FabIndia, a prominent retailer, has announced that it is facing sluggish sales and trying to negotiate with its landlords for reduced rental charges, as a cost-cutting measure. The consumer sentiment is the worse now that despite a 50%-70% discount offer, the sales are not improving. Lifestyle has said that their walk-ins have dropped by 3-5%.

I was just wondering, if together all these pieces of information are trying to convey that we are heading for a recessionary environment. Are such weak domestic business activity combined with global slowdown, escalating trade tensions? Does this unconventional move by RBI, is signalling that Government is preparing for a downturned economic situation? Possibly yes, with various economic indicators also leading to similar conclusions: (a) CRISIL lowered the GDP growth forecast by 0.20% to 6.90% for FY20; (b) Weak monsoons this year; (c) Global growth is limping too; (d) Slow growth in industries.

If one ventures onto understand what might be the possible reasons for such gloomy situation, it does not seem to be just one of the event/reason, nor it seems to be a simple economic cycle repeating itself, in its natural trend. Let me quote few reasons, what I feel might be causing this:

Firstly, demonetisation drive of November, 2016. While without an argument, I do believe there needed a blow to the increased parallel economic activity in the country, a situation like this as a side effect of such move was inevitable, with the question being not if, but when. A blow to black money, also resulted as a blow to consumption, household income, revenue models of unorganised small and micro business segment, growth in rural wages and of course employment generation.

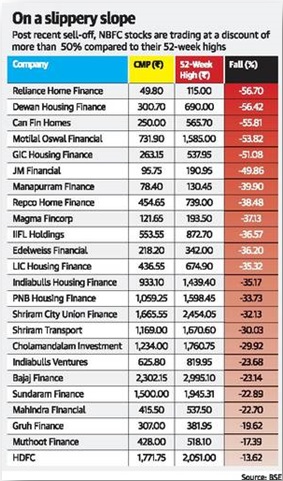

Thirdly, the NBFC credit crisis erupted with IL&FS, a leading lender to infra sector, declaring defaults in its repayment of borrowings from Banks. This created a panic mood in market, with rating agencies lowering the credit rating for IL&FS. This triggered critical investigation into the lending and borrowing patterns of other NBFCs also (likes of Indiabulls, Piramal Group and DHFL), and it could easily be concluded that NBFCs have resorted to the model of rolling over debt and just sailing through for the day, with the hope of “someday in future” all their problems be resolved. A perfect simile for Lehman Brothers situation just before 2008 crisis.

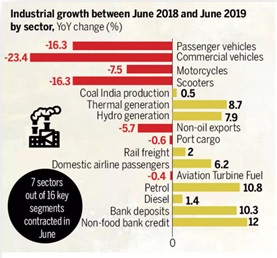

Fourthly, the tight monetary policy since last four years, with single-minded focus of GOI to bring down the fiscal deficit. With maintaining a hard interest rate situation in the economy, and a highly controlled inflation rate, (which in turn had alternative effects on the industrial and agricultural production and sales), all that the economy could gain is a drop of fiscal deficit from around 3.5% in 2016-17 to 3.3% in 20018-19. Economy must be thinking, was it even worth to sacrifice few basis points of growth to achieve just about a 0.20% reduction of fiscal deficit. The non-food inflation has been higher than the food inflation. Due to which the income flow has moved to urban areas and rural areas have suffered. This is reflected in the poor urban wage scenario.

Fifthly, global market outlooks, constantly maintained a poor picture, with US-China trade war, BREXIT effects, and expectations of crude oil prices rising. These reduced the aggression in the export oriented business owners.

Sixthly, the stock markets are also not adding to economic confidence. FIIs have pulled more than Rs. 12000 crores out of Indian markets (cited reasons being the higher tax surcharge on super-rich) in July 2019 alone.

I have just tried to connect events and news to make sense out of it. And yes, it seems that the slowdown is down the corner, or maybe we are already hugging the bear. Way forward demands cautious moves. Governmental policy decisions, will have very high impact on the economic situation. Thankfully, a majority government in centre is of great help for firm and quick decisions. Investors in the markets need to resort to fundamentalist investment strategies with long-term orientation, and a staggered investment patterns. Its time that Indian businesses start adopting serious risk management initiatives to manage their price risks – hedging should become a compulsory business process. Banking and NBFC sector will play a major role in economic sustainability. In addition to be cautious in lending and borrowing, these institutions also need to adopt newer default risk management products, that include asset backed securities and other financial reengineered processes.

Despite the gloomy mood, the fact that the fundamentals of Indian economy and financial markets are strong and attractive, be it in the consumer demand, comparative advantage over labour and certain natural resources and the sharp business acumen of Indians, continue to be the drivers of economy in the long-run. Its just about handling a negative phase in the short-run.

Disclaimer: The views, opinions and content on this blog are solely those of the authors. ISME does not take responsibility of content which are plagiarized or not quoted