Medium Link: https://medium.com/@geetaashok/banking-on-green-7737dcde1a2c

Course Relevance: Banking Law and Practice – BBA 5th Semester

Academic Concepts: Fiduciary duty of banks to safeguard stakeholder interests (depositors, investors & society), Know Your Customer (KYC) and Enhanced Due Diligence (EDD) for polluting industries, Paperless banking (UPI, e-KYC, digital onboarding), Energy-efficient data centres, Green deposits, Green bonds, AI for risk detection in climate-sensitive sectors

Teaching Note: This caselet will help students understand the legal and regulatory framework governing green banking in India. It will explain how sustainability fits into banking operations, products, and risk management. Thus students can develop a responsible banking mindset and appreciate the evolving role of banks as environmental stewards. The students can apply Banking Law concepts to evaluate whether banks fulfil fiduciary duties while lending to environmentally sensitive projects.

Learning Objectives:

The students will be able to:

- Describe key concepts such as ESG, climate risk, environmental due diligence, and sustainable finance in the context of banking law and practice.

- Identify the green banking initiatives and sustainability strategies adopted by major Indian banks.

- Compare sustainability reporting practices across banks and assess their level of compliance with regulatory and legal standards.

- Analyse how environmental and climate risks influence credit appraisal, loan pricing, and risk management under banking law.

Banking on Green:

Top 5 Indian Banks Powering the Sustainability Revolution

Climate-aware finance isn’t a niche anymore. It is becoming the backbone of long-term banking strategy. In India, where development needs collide with pressing climate goals, banks are uniquely positioned to channel capital into low-carbon infrastructure, renewable energy, green buildings, and sustainable livelihoods.

Why green finance matters?

Green finance means financial products and services that support projects with environmental benefits such as renewable energy, energy efficiency, clean transport, water and waste systems, sustainable agriculture, and more. A robust green finance ecosystem helps countries decarbonise without choking development by aligning capital flows to climate objectives. In India, the green finance market has grown rapidly in recent years, including green bonds, sustainability-linked loans, and project financing aligned to climate goals; tracking these flows is now a national priority as the country scales climate action at pace.

The Top 5 Indian Banks Leading in Green Finance and how they’re driving the transition

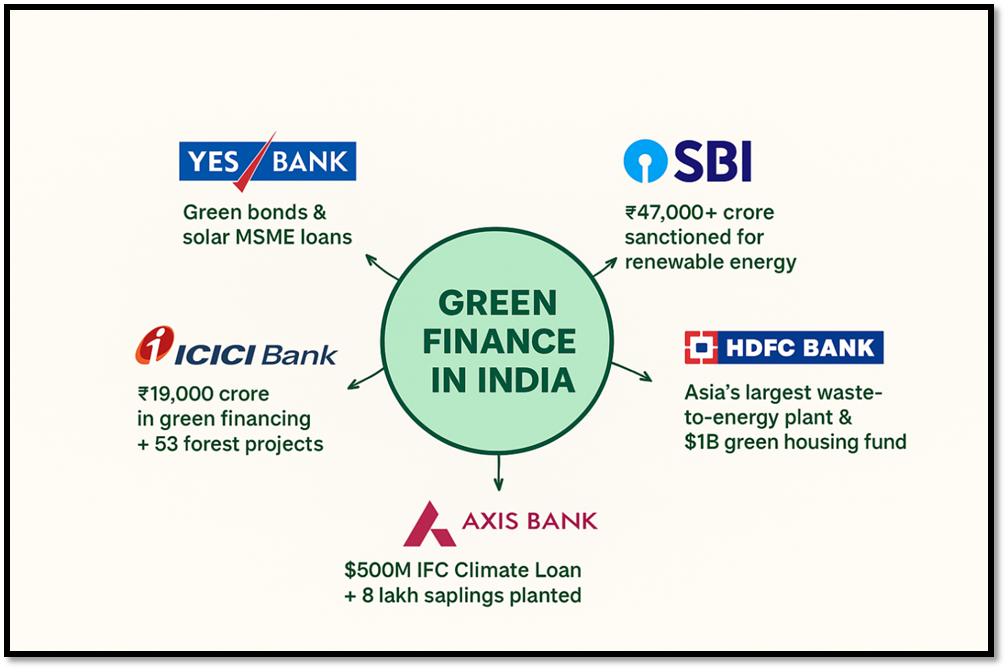

There are five Indian banks that are widely recognised for leading the charge in green finance: YES BANK, State Bank of India (SBI), ICICI Bank, Axis Bank, and HDFC Bank. There are many Indian banks making sustainability efforts, but these five stand out for a mix of scale(large project finance footprints), credentials (green bond issuance and frameworks), public commitments (net-zero targets or green targets), and reporting/transparency (detailed sustainability or impact reports). Together they represent a mix of public and private sector banks that are shaping market standards and products for green finance in India. Here is a summary of each bank’s main green initiatives which offers a critical lens on strengths and limitations.

- YES BANK — The early mover and green-finance brand

YES Bank has been one of the earliest private sector banks to champion the green finance agenda in India.

Solar Lending for MSMEs: Through its YES Kiran programme, the bank offers financing support to small and medium businesses that wish to adopt solar energy solutions. The scheme not only provides loans but also partners with leading solar manufacturers to ensure that clients receive reliable technology and easy access.

Support for Clean Technology Start-ups: With its YES Scale Cleantech Accelerator, the bank has given young businesses working in renewable energy, waste management, and water conservation access to mentoring, funding, and market linkages.

Green Bond Initiatives: YES Bank has frequently used the bond market to raise money for sustainable infrastructure and renewable energy. For example, it raised roughly ₹330 crore via FMO and earlier issued bonds in collaboration with IFC. These monies have been directed into solar and wind power projects across the country.

In summary, YES Bank is actively creating an ecosystem for India’s green economy in addition to lending money.

What they’re doing: YES BANK has long positioned itself as a specialised sustainable finance bank, developing dedicated green financing products (renewable energy, electric vehicles, rooftop solar, green working capital), issuing green bonds, and publishing detailed sustainability disclosures and targets. Their sustainability strategy explicitly channels capital to climate solutions and they’ve received high sustainability ratings in global assessments.

Why it matters: YES BANK’s brand identity now ties strongly to climate finance. That matters because leadership by branding influences peers. When a major bank packages green loans at scale and publicly reports impact metrics, it creates market signals (pricing, risk frameworks, reporting templates) that other banks can adopt. YES BANK’s early focus on green products has helped standardise eligible project categories and create practical loan documentation for renewable energy and energy efficiency projects.

Strengths: Early mover credibility, product innovation (e.g., targeted SME rooftop solar financing), visible sustainability reporting and external recognitions.

Limitations/Watch-outs: Market scale relative to larger public and private sector banks is smaller; sustained impact requires continuing strong asset quality and capital resilience while scaling climate portfolios.

2) State Bank of India (SBI) — Scale with Public Leadership

As the country’s largest public sector bank, SBI’s sustainability drive has a wide impact.

- Global Green Bond Issuances: In 2024, SBI raised USD 250 million through green bonds from its London branch. The proceeds are dedicated to projects like clean energy, efficient transport, and climate adaptation measures.

- Renewable Energy Loans: By March 2024, the bank had sanctioned over ₹47,000 crore towards solar, wind, and other renewable energy projects.

- Future Commitments: SBI has committed that by 2030, at least 7.5% of its total loan bookwill be linked to green and sustainable finance.

- International Partnerships: Its collaboration with Agence Française de Développement (AFD) at GIFT City brought €100 million for climate-friendly projects.

- Community Green Projects: SBI is also active in environmental CSR. For instance, its SBI Jan-Van initiative converted arid land at MGRDPR University, Karnataka, into a green zone with solar installations and water harvesting structures.

SBI’s massive scale ensures that its sustainability efforts ripple through both urban infrastructure and rural communities.

What they’re doing: SBI, India’s largest lender by assets, has rolled out a sizable green agenda: green bond issuance, a dedicated ESG & Climate Financing Unit, and public commitments to increase the share of green advances in its loan book. SBI has stated targets for green advances and initiated frameworks to align lending to climate outcomes — including post-issuance reporting and impact analysis for green bond proceeds.

Why it matters: Scale. When the country’s largest bank sets targets such as channeling a defined proportion of gross advances into green projects, it influences the whole market. SBI’s underwriting standards and risk assessments also matter for project bankability — especially for large infrastructure and municipal projects that require syndicated funding or long tenors.

Strengths: Unmatched balance sheet size and distribution (can finance big-ticket renewable and municipal infrastructure deals); institutional role in public-private partnership financing.

Limitations/Watch-outs: with scale comes complexity: aligning a vast and diverse loan book to “green advance” metrics is an operational challenge. Public sector banks also face governance and asset-quality dynamics that can complicate long-term green lending.

3) ICICI Bank — Private sector scale and integrated disclosure

ICICI Bank has built sustainability into both its business and operations.

- Environmental Restoration Projects: Through ICICI Foundation, the bank has supported conservation initiatives in over 50 wildlife sanctuaries and forests across 19 states. These efforts include watershed development, afforestation, and livelihood support to local communities.

- Green Building Practices: Many of ICICI’s offices and data centres have achieved Indian Green Building Council (IGBC) ratings. In FY2024 alone, more than half a million square feet of its new spaces were certified for their eco-friendly design.

- Climate-Aligned Lending: The bank is consciously expanding its “green lending” book. By 2024, around ₹19,000 crore was committed to renewable energy and climate-aligned sectors, making up nearly half of its sustainability financing portfolio.

- Reducing Operational Emissions: Apart from lending, ICICI has been cutting its own carbon footprint by adopting renewable energy sources, minimizing waste, and promoting digital banking to reduce paper use.

This dual approach—financing sustainability while practicing it in-house—makes ICICI a standout in green banking.

What they’re doing: ICICI Bank has advanced sustainable financing through an institutional Sustainable Financing Framework, expanded disclosures of green loans and related activities, and operational commitments such as carbon-reduction targets and financing for renewables, EVs, and green industry. In recent reporting cycles the bank has expanded what it counts as renewable-energy-associated financing — moving beyond pure project loans to include manufacturing and value-chain actors.

Why it matters: ICICI brings private-sector agility combined with the ability to underwrite large corporate deals. Their approach to disclosure and to expanding eligible activities matters for how the private financial sector defines and reports green finance (e.g., manufacturing of renewable components, EPC contractors).

Strengths: Robust ESG disclosures, product diversity, private sector risk management frameworks.

Limitations/Watch-outs: Private banks may pursue sustainability-linked products that risk being headline-driven unless backed by strict KPIs and independent verification.

4) Axis Bank — Green bond issuer with transparent impact reporting

Axis Bank has steadily expanded its climate commitments, both globally and locally.

- Climate Loan from International Finance Corporation: In 2024, Axis Bank secured a $500 million facility from the International Finance Corporation to strengthen financing for renewable energy, water conservation, green buildings, and marine ecosystem protection.

- Green Home Loan Partnership: With Mahindra Lifespaces, Axis Bank now offers discounted loans to customers purchasing certified green homes, making sustainable living more affordable.

- Internal Sustainability: The bank’s headquarters, Axis House, in Mumbai, showcases water harvesting, recycling, and energy-efficient operations. Digital banking initiatives further help in reducing paper usage.

- Tree Plantation & Restoration: In 2023 alone, Axis planted over 800,000 saplings, supporting biodiversity and habitat restoration. It has also initiated solar cold storage units in rural India to help farmers cut food wastage.

- Awareness Campaigns: Through its “Open for the Planet” and “Clean-A-Thon” initiatives, Axis Bank has mobilized employees and citizens to clean public spaces and water bodies.

Axis Bank blends financing with grassroots environmental action, creating impact at multiple levels.

What they’re doing: Axis Bank has been active in issuing sustainable bonds and publishing comprehensive impact reports linked to sustainable finance frameworks. Their public reporting offers line-level details on eligible green projects and impact accounting (e.g., renewable capacity financed, emissions avoided estimates), and they have a formal Sustainable Financing Framework aligned to market expectations.

Why it matters: Axis Bank’s structured approach to bond issuance and impact disclosure helps drive investor confidence in India’s GSS+ (green, social, sustainability and sustainability-linked) debt market. Transparent use-of-proceeds reporting reduces greenwashing risk and improves the pricing and uptake of green debt instruments in domestic and international markets.

Strengths: Disciplined reporting, sizeable project pipelines in renewable energy and related infrastructure.

Limitations/Watch-outs: Investor expectations for standardised impact metrics keep evolving; banks must continue harmonising reporting to international standards (e.g., ICMA Green Bond Principles, Climate Bonds).

5) HDFC Bank — Retail reach and green product platforms

HDFC Bank is embedding sustainability into its long-term growth strategy.

- Funding Waste-to-Energy Projects: One of its most significant contributions is financing Asia’s largest municipal waste-to-energy plant in Indore, which converts over 500 tonnes of waste into compressed biogas and compost daily.

- Clean Energy Access in Villages: Under its flagship ‘Parivartan’ programme, the bank has already set up over 60,000 solar streetlights, water supply systems, and solar irrigation pumps across 22 states. By 2025, it plans to bring renewable energy solutions to at least 1,000 villages.

- Green Housing Finance: Through a joint initiative with IFC, HDFC Capital has launched a $1 billion fundto promote affordable green housing, ensuring that low-cost housing is also sustainable.

HDFC Bank’s initiatives reflect a clear belief that rural inclusion and urban innovation must go hand-in-hand in building a greener economy.

What they’re doing: HDFC Bank has integrated sustainability into lending practices and built sustainable finance frameworks to support green loans, retail green products, and corporate lending aligned to environmental outcomes. While historically known as a leading housing finance provider (through its group), HDFC Bank is leveraging its massive retail and SME footprint to introduce green retail offerings (e.g., green home loans, green vehicle finance) and to support green project finance.

Why it matters: Reaching consumers and small businesses is essential for a low-carbon transition. When large retail banks make green home loans or EV loans accessible and competitively priced, adoption accelerates at the grassroots level.

Strengths: Deep retail distribution, product innovation potential for green consumer finance.

Limitations/watch-outs: Assessing the climate impact of retail-scale loans requires robust tracking and sometimes small incremental emissions gains per loan — aggregating these up and reporting credibly is still an emerging practice.

Common themes across the five banks

- Frameworks + reporting are now table stakes. Each bank has a sustainable finance framework that defines eligible categories and reporting commitments. That’s critical for investor confidence and market growth.

- Green bonds and GSS+ debt are catalysts. Green and sustainability-linked instruments are a principal mechanism for channeling capital, and India’s sustainable debt market has expanded rapidly, encouraging banks to scale up green pipelines.

- From project finance to value chain finance. The focus is broadening: not just financing renewable projects but also manufacturers of clean energy components, EPC contractors, and downstream services — which increases the leverage of green finance across sectors.

- Operational emissions matter, too. Banks are setting targets for their own Scope 1 and 2 emissions and starting to account for financed emissions (Scope 3), though methodologies and timelines vary.

Critical Questions & Challenges:

- Additionality vs. Labeling: Are banks financing projects that wouldn’t happen otherwise, or simply refinancing existing projects under a “green” label? Transparent post-issuance impact verification can help answer this.

- Standardisation of Metrics: Metrics for impact (e.g., tCO₂ avoided per rupee) vary; better alignment with international standards would improve comparability.

- Financing Inclusivity: Green finance must reach beyond marquee renewable projects to SMEs and municipal services in smaller cities and rural areas — that’s operationally harder but essential for equitable transition.

- Transition Finance: Banks need strategies for decarbonising “brown” sectors (e.g., heavy industry) through transition finance, structured appropriately to avoid lock-in.

Conclusion:

Green finance in India is moving from pilot projects and brand statements to a structural element of bank strategy. The five banks profiled here — YES BANK (an early specialised leader), SBI (public sector scale), ICICI Bank (detailed private-sector reporting and expanded eligible categories), Axis Bank (focus on green bonds and impact reporting), and HDFC Bank (retail reach and product potential) — exemplify different pathways to leadership. Together they demonstrate that green finance requires credible frameworks, transparent impact reporting, product innovation, and the will to mobilise capital at scale.

For researchers, the frontier lies in assessing quality (did financed projects genuinely reduce emissions?) and equity (did finance reach the communities that need it?). For banks and policymakers, success will be judged not by headline green volumes alone but by measurable climate outcomes and inclusive access to finance for the transition.

To conclude, banks like SBI, HDFC, PNB, ICICI, and Axis are proving that banking and sustainability can go hand in hand. They are financing renewable energy, offering green products, and running their operations responsibly.

This is very clear from the following anecdote. A farmer in Maharashtra recently installed solar pumps through a green loan scheme. He said something simple but profound: “Earlier, I depended on rain and diesel. Now, I depend on the sun. My children’s future is brighter.” That farmer’s words reminds us of a powerful quote by former UN Secretary-General Ban Ki-moon:

“There is no Plan B because we do not have a Planet B.”

Caselet Questions:

- State Bank of India has been actively involved in promoting green financing. In 2023, SBI raised a significant amount through green bonds. What was the amount raised, and what were the primary areas targeted for investment?

- HDFC Bank introduced a unique financial product aimed at promoting sustainable investments. What is the name of this product, and how does it contribute to environmental sustainability?

- ICICI Bank has been involved in raising funds through green bonds. How much did the bank raise, and what is the intended use of these funds?

- Axis Bank has been recognized for its efforts in promoting green banking. Can you mention at least two initiatives the bank has undertaken in this regard?

***************************************************************************