Investors attempt to optimize in a particular manner as proposed by Harry Markowitz’s Modern portfolio theory. And that manner is referred to by him as rationality. According to the theory, rational behaviour is warranted as investors are led to decide in uncertainty. Investors wanting to earn the maximum return is as rational as sun rising in the east. Since the return on a risky asset depends on values that various market and asset variables can take in future and the future is unknown, it becomes imperative that rational behavior of investor also considers risk of investing. A risky asset with higher expected volatility is bound to be under-preferred by the rational investor versus a risky asset with comparatively lesser expected volatility. The crux of efficient portfolio theory as per Markowitz, thus, becomes the efficient frontier, essentially a Pareto line optimizing in two dimensions – expected return and the variance of such return (Markowitz H. M., 1990). Also, it can be noted that expected return is a desirable thing and variance of the return is an undesirable thing. (Markowitz H. , 1952)

Therefore, the process of portfolio building is, evidently, aiming to earn maximum possible return, while anchoring the risk parameter. Maximizing the anticipated return is a function of different variables estimated and used in the valuation process. Whereas, curbing the risk in the portfolio requires defining the risk in the first place. First, the asset class risk – that is hovering around the class of the asset as a whole; second, the security-specific risk – that’s the sensitivity of the security’s returns to changes in prices of the benchmark portfolio. The asset class risk can be brought down by diversifying across different classes of assets. Similarly, portfolio-specific risk can be reduced by different portfolios with directional movements that are divergent from each other.

The portfolio theory of Markowitz has well established that the security-specific risk can be brought down with ease by constructing a portfolio with an optimum proportion of a set of securities between whom the co-linearity is minimum. A mutual fund is supposed be a tool that can work in this direction, for an investor, who wishes to rely on the professional to take up the risk management task. Every mutual fund theoretically and practically is a diversified portfolio and supposed to be bringing down the volatility factor for the investor, as compared to a singular investment decision. And because, mutual funds take care of the security-specific risk, to a large extent, the risk that investors may have to focus would be the asset-class risk or the market risk.

It is well established that a rational investor would choose a combination of risk-free rate (defined as the rate in the absence of demand for any risk premium) and risk premium, through the seminal contributions of William Sharpe. Sharpe raised the question on the relationship between the risk and return of a portfolio and developed an asset pricing model that focused entirely on building a portfolio that minimized the difference between the marginal utility of investing in any security in a given portfolio. This was achieved by quantifying the assumed linear relationship between the expected returns on securities and their covariance with the market portfolio, viz., beta. (Sharpe, 1990). The beta could be obtained by,

………………Equation-1

Where, is the beta of the security or portfolio i, is the covariance between the security or portfolio i and the market portfolio and is the variance of the market portfolio. This was proliferated with the risk premium demanded by the investor to satisfy his utility function (which in turn depended on his risk appetite) and the combination of beta adjusted risk premium and the risk free rate became the expected return on a security or the portfolio.

By combining the efficient frontier and the expected return arguments, it could be inferred that market portfolio is supposed to be efficient and there exists a linear relationship between expected return and beta. And this becomes the strong argument in favour of mutual fund managers, theoretically speaking. Given that mutual funds are able to manage the unsystematic risk – as measured by their reduced variances of returns, are they also able to manage the systematic risk? Note that, there is no way one can target to reduce the systematic risk, but, the fund can deliver a return that is on par with the expected return of the investor (again, as measured by the investor’s risk appetite).

Thus, this study aims to test if mutual funds in the Indian context, have been able to successfully generate a return that is in line with investor expectations. The objective of this study is to investigate whether fund managers of Indian mutual funds are efficient in managing the total risk and the unsystematic risk.

Study Design

A sample of 35 Indian mutual funds were selected based on judgmental sampling. Judgmental as the funds were selected to capture almost all the fund houses in India (listed as per Value Research Online (Value Research Online, 2017). Also, diversified equity funds, multi-cap funds, large cap funds and high one year annualize return earned funds, in the pecking order were s

elected such that, there is a representation of one fund at least from each fund house. Due to availability of data and reliability study conducted, we could restrict our sample size to 29 funds.

The data is collected directly from the reported fund factsheets published by each fund house in their websites’ downloads section. The fact sheets of the month of December-2016 are sued for the computational purposes. The data pertains to REGULAR GROWTH option of each fund. Standard deviation figures are annualized. Beta values are based on past three years of historical Net Asset Values.

The analysis is carried out by following process:

Step-1: Computation of return on each of the sample mutual fund, assuming mutual fund managers (who are essentially the investors in this case) behave rationally, and thus, the fund returns fall on the efficient frontier. In other words, assuming mutual fund portfolios and the market index portfolio are efficient portfolios, investing in any of this portfolio would provide a maximum return for the investors, while holding the risk at desirable level. This is computed using the Capital Market Line Equation:

………………Equation-2

Where, is the expected return on efficient portfolio j, is the risk-free rate, is the slope of the capital market line, and is the standard deviation of the portfolio j.

The slope of the Capital Market Line is obtained using the equation given by:

………………Equation-3

Where, is the slope of the Capital Market Line, is the expected return on market portfolio, is the risk-free rate and is the standard deviation of the market portfolio returns.

Step-2: As the objective of the study is to see whether Indian mutual fund managers are efficient in managing the non-diversifiable risk, which is represented by the CML equation return as computed in table-2 above, it would also be necessary to compare the returns of those portfolios, which do not necessarily fall on the efficient frontier. The expected return and the standard deviation of such portfolios should be falling below the CML, as these are inefficient and not purposefully well-diversified. Such portfolios exhibit linear relationship between their expected returns and covariance with the market portfolio, but, need not give a conclusive pattern of such relation (Chandra, 2012). Such relationship will result in an expected return as given by:

………………Equation-4

Where, is the expected return on inefficient portfolio i, is the risk-free rate, is the slope of the inefficient portfolio with that of the market portfolio (which is supposed to be efficient with β = 1) also called the slope of the Security Market Line (SML), and is the covariance of the returns of inefficient portfolio and the efficient market portfolio. The is computed by:

………………Equation-5

Where, is the slope of the SML, is the expected return on market portfolio M, is the risk-free rate, is the variance of the market portfolio M.

Presented below is the table (Table-4) summarizing the expected returns (of both CML and SML explanation) and the actual return of the funds:

If the CML and SML were to determine fund manager behavior, there must exist a statistically significant difference in the mean values of returns between the two series of returns. We connote to represent the difference between fund’s actual return and expected return based of firm’s total risk (i.e., standard deviation) and to represent the difference between fund’s actual return and expected return based of firm’s unsystematic risk (i.e., beta); Therefore, below hypothesis can be tested:

H0:

(Null Hypothesis: There is no statistically significant difference between the mean excess returns of mutual fund portfolios under CML and SML)

H1:

(Null Hypothesis: There is a statistically significant difference between the mean excess returns of mutual fund portfolios under CML and SML)

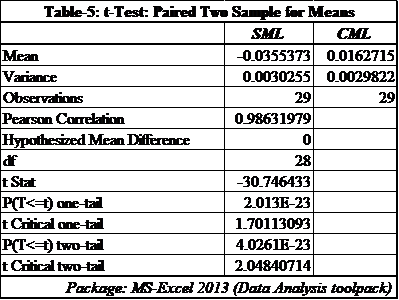

The t-test for paired two sample for means is conducted and the results are presented below (Table-5)

As the p-value of the t-test for hypothesized mean difference in two variables is less than 0.05 (alpha value for 95% level of confidence), we reject the null hypothesis that there is no statistically significant difference between the mean excess return given by total risk management efficiency and unsystematic risk management efficiency. Thus, we infer that there does exist a statistically significant difference in the mean excess return given by two approaches. Combining the hypothesis test result with that of the graphical presentation before, we can induct that mutual fund managers are efficient in managing the unsystematic risk, which in any case, the proof of Markowitz’s modern portfolio theory, whereas the question, whether, fund managers can be more efficient than the market itself, could not be answered, as no pattern could be established.

Conclusion

With the objective of testing whether Indian mutual fund managers are efficient in managing their respective portfolios such that benefits of diversification are delivered and also an excess return is generated to compensate for the asset-class risk assumed by the investor. The discussion on modern portfolio theory, asset pricing models and market efficiency gave the direction to design the testing process. The 29 Indian mutual funds those were selected have been used to determine the excess returns generated by them, over and above the expected returns. There were two such approaches used. One, total risk was taken as a base to determine the expected return, with the assumption that investors, expect mutual funds to compensate with higher return for the total risk that they take. Capital Market Line equation was used for the same. Two, non-diversifiable risk was taken as a base to determine the expected return, with the assumption that investors are rational enough to understand that markets are so efficient that no investor could earn an excess return than the market. Hence, the expected return was arrived at by adjusting for the unsystematic risk assumed by the investor. Security Market Line equation served this purpose. We also tested the hypothesis for difference in the mean excess returns under two approaches, and concluded that there did exist a statistically significant difference between the two.

Thus, we conclude that Indian mutual fund managers are indeed managing the funds efficiently in terms of bringing down the overall risk of investing in equity securities for the retail investors to the extent of the unsystematic risk. This is a proof for the Markowitz’s theory of diversification (Markowitz H. , 1952). Does it mean fund managers are doing great job? Not really. From this study we did find that there is ample scope for the fund managers to design portfolios that can bring down the systemic risk (Total risk minus unsystematic risk), which would be possible with various other investing strategies ranging from value investing to contra investing.