Are Indian Banks Heading Towards ‘Financial Embarrassment’?

– Kiran Kumar K V

Box 1:The Economic Times 27-June-2015 |

also ensures to sound confident on the prospects of India and Indian Banks despite the external influences like these.

While the Central Bank and the Government will dwell upon to ensure the external risks of the above-kind, the banks per se, operating in India need to ensure that they are operationally covered to sustain themselves. Ceteris paribus, especially the external risks, how do the Indian banks cope with distress?

Objective of this Analysis: This analysis aims to test the possibility of Commercial Banks in India going bankrupt in the next 2-3 years, purely based on their operational efficacy.

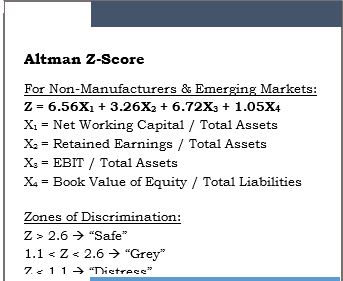

Box 2: Altman Z-Score Formula |

|

Analysis & Results: Constituents of BSE Bankex Index were taken as sample (12 banks), data pertaining to their financials were collected from their respective annual reports for the year ended 31-March-2015 and requisite ratios and Z-Score are computed. The data and their computations are presented in the below table (Box-3)

(Figures In) | Total Assets | Working Capital | Retained Earnings | Earnings | Equity | Total Liabilities | |

TA | NWC | RE | EBIT | EQ | TL | ||

Bank Of India | In Lakhs | 62528474 | 502170 | 3185720 | 754949 | 3252285 | 4009869 |

Axis Bank | In Crores | 467243 | 60163 | 44475 | 7358 | 44950 | 84394 |

Bank Of Baroda | In Crores | 676114 | 11076 | 37416 | 4931 | 37847 | 36976 |

Canara Bank | In Crores | 553152 | -26040 | 26611 | 2703 | 27086 | 25763 |

Federal Bank | In Crores | 82908 | -2474 | 7529 | 1012 | 7700 | 2393 |

HDFC Bank | In Crores | 607097 | 37433 | 62653 | 10216 | 63154 | 59478 |

ICICI Bank | In Crores | 826079 | 109891 | 83537 | 11175 | 84697 | 211252 |

Indusind Bank | In Lakhs | 10911592 | 1767533 | 1010103 | 309822 | 1063048 | 2061806 |

Kotak Mahindra Bank | In Crores | 148561 | 42639 | 21752 | 3065 | 22138 | 31415 |

Punjab National Bank | In Crores | 636011 | 19757 | 42217 | 3341 | 42588 | 59205 |

State Bank Of India | In Crores | 2700110 | 51323 | 160641 | 17517 | 161388 | 244663 |

Yes Bank | In Crores | 136170 | 14279 | 11262 | 1997 | 11680 | 26220 |

Box 3: Financial Data of BSE Bankex Constituents

are presented in the below chart (Box-4)

Box 4: Altman Z-Score for BSE Bankex Constituents

Kotak Mahindra Bank and Federal Bank were found to be in safe zone. Canara Bank and State Bank of India are in distress zone. All other banks are in the grey zone. Going by Altman’s model we may predict distress zone banks to go into bankruptcy in the near future; grey zone banks need to exercise caution and relook into their operational strategies; whereas banks in safe zone need to maintain status quo.

In the context of a probable economic downturn, as discussed above and when considered as a whole, it can be observed that most of the banks in India fall under grey zone, which is not so immune state to be in, (even though it’s not a distress state).

Conclusion:The above results need to be viewed with caution, as Altman model is developed primarily on manufacturing firms and applicability of the same on non-manufacturing firms, especially banking and financial firms are yet to be proven by researchers[3]. Lack of literature on the same is a big limitation for this analysis. As an academic attempt, this study can remain as a record and unfolding of the future can lead to further research in the area and development of a model meant for banking companies.

There is no evidence to suggest computation of a Z-Score is a better means of analysing long-term solvency. Rather, it can be asserted that use of these ratios as predictors of distress is best in complementing a rigorous analysis of financial statements. Evidence from literature does suggest the Z-Score is a useful screening, monitoring and attention-directing device.[4]

Going by the results, it can be concluded that banks of India, have as an undercurrent, a not-so-satisfactory operational efficacy, and unless these are fixed for better, financial embarrassment – in the event of Mr. Rajan’s prediction coming true – is something that could be a reality.

[1] (Economic Times Mumbai Bureau, 2015)

[2] (Altman E. I., 1968)

[3] (Altman Z-Score, 2015)

[4] (Wild, Subramanyam, & Halsey, 2007)

Altman Z-Score. (2015). Retrieved from Wikipedia – The Free Encyclopedia: https://en.wikipedia.org/wiki/Altman_Z-score

Altman, E. (2000). Predicting Financial Distress of Companies: Revisiting the Z-Score and ZETA Models.

Altman, E. I. (1968). Financial Ratios, Discriminant Analysis and the Prediction of Corporate Bankruptcy. Journal of Finance.

Economic Times Mumbai Bure

au. (2015, June 27). Rajan Rings the Alarm Bell: Chances of Global Depression. The Economic Times, p. 1. Retrieved from http://epaperbeta.timesofindia.com/Article.aspx?eid=31815&articlexml=Rajan-Rings-the-Alarm-Bell-Chances-of-Global-27062015001030

au. (2015, June 27). Rajan Rings the Alarm Bell: Chances of Global Depression. The Economic Times, p. 1. Retrieved from http://epaperbeta.timesofindia.com/Article.aspx?eid=31815&articlexml=Rajan-Rings-the-Alarm-Bell-Chances-of-Global-27062015001030

Wild, J. J., Subramanyam, K. R., & Halsey, R. F. (2007). Credit Analysis. In J. J. Wild, K. R. Subramanyam, & R. F. Halsey, Financial Statement Analysis (pp. 540-541). Tata Mc-Graw Hill.