~~

Beginning of the Case ~~

Beginning of the Case ~~

A LOT

IS HAPPENING OVER A COFFEE..!!!

IS HAPPENING OVER A COFFEE..!!!

(Case Study – Valuing

IPO of Café Coffee Day)

IPO of Café Coffee Day)

Swarup

prefers to spend his Sundays as dull as possible. The Sunday of October 11th

of 2015 was going to be different for him. On any other weekday he would’ve commenced

the day with getting a global market update from the Bloomberg app on his iPad.

Being an investment broker for several HNI investors of Equate Advisors, Swarup

is a much sought after relationship manager by his clients. His clients feel Swarup

is one such adviser, whose stock picks rarely go wrong. His boss at Equate

Advisors is generally happy with his performance in terms of delivering numbers

and maintaining satisfied customer relations, but, he feels Swarup sometimes

contradicts the stock advises of central research team. Swarup argues that’s

precisely the reason for his success. He does not blindly recommend a stock to

his clients, instead, with every such recommendation that comes to him from his

research team in Mumbai, he does his own valuation of the stock before he

arrives at his conclusion. He strongly believes this always works.

prefers to spend his Sundays as dull as possible. The Sunday of October 11th

of 2015 was going to be different for him. On any other weekday he would’ve commenced

the day with getting a global market update from the Bloomberg app on his iPad.

Being an investment broker for several HNI investors of Equate Advisors, Swarup

is a much sought after relationship manager by his clients. His clients feel Swarup

is one such adviser, whose stock picks rarely go wrong. His boss at Equate

Advisors is generally happy with his performance in terms of delivering numbers

and maintaining satisfied customer relations, but, he feels Swarup sometimes

contradicts the stock advises of central research team. Swarup argues that’s

precisely the reason for his success. He does not blindly recommend a stock to

his clients, instead, with every such recommendation that comes to him from his

research team in Mumbai, he does his own valuation of the stock before he

arrives at his conclusion. He strongly believes this always works.

By

the time he woke up on this Sunday it was already 9.30 am. He stepped out of

his apartment after a short work-out module at the club-house. The

generally-residential area that it is, Sahakar Nagar in Bangalore, was

semi-urban in landscape. Less than 200 meters from his apartment complex was an

outlet of Café Coffee Day (popularly

called CCD), to which Swarup was a regular visitor. He had an emotional connect

with CCD, as most of his successful client meets happen in CCD outlets, thanks

to widespread presence across Bangalore; he spends most of his leisure and he

feels rejuvenated after every visit in CCD; and more than anything, it is in

this CCD that he proposed his girlfriend (and she accepted..!!). Truly a lot

happened to Swarup over Coffees in CCD…!!!

the time he woke up on this Sunday it was already 9.30 am. He stepped out of

his apartment after a short work-out module at the club-house. The

generally-residential area that it is, Sahakar Nagar in Bangalore, was

semi-urban in landscape. Less than 200 meters from his apartment complex was an

outlet of Café Coffee Day (popularly

called CCD), to which Swarup was a regular visitor. He had an emotional connect

with CCD, as most of his successful client meets happen in CCD outlets, thanks

to widespread presence across Bangalore; he spends most of his leisure and he

feels rejuvenated after every visit in CCD; and more than anything, it is in

this CCD that he proposed his girlfriend (and she accepted..!!). Truly a lot

happened to Swarup over Coffees in CCD…!!!

He

walked into the shop ordered his regular cappuccino with butter cookies and unlocked

his iPad

walked into the shop ordered his regular cappuccino with butter cookies and unlocked

his iPad

screen, while still being amused at the young crowd at the shop

already barged in. The moneycontrol.com

website that he had open yesterday was still on the first screen. As if it was

usual, Swarup reluctantly glanced through news stream, and he found a news item

– “Café

Coffee Day to go Public”. He also recalled grapevine download from his

chitchat with his research team that Equate Advisors are going to recommend CCD

for a buy at IPO aggressively. His hot espresso was served and he could just

smile at the thought of how hot CCD’s IPO going to be. He decided to be better

prepared. And this Sunday was to become a working Sunday for him.

Swarup

believes valuing a stock means valuing a business. It’s important to understand

the fundamental business model of the company. He browsed through the red

herring prospectus (RHP) of the company and few websites to gather relevant

information and made notes as below, as he usually does:

believes valuing a stock means valuing a business. It’s important to understand

the fundamental business model of the company. He browsed through the red

herring prospectus (RHP) of the company and few websites to gather relevant

information and made notes as below, as he usually does:

i.

Stakeholders: CCD’s parent company

Coffee Day Enterprises Limited (CDEL) is held by V G Siddarth-led promoter

group upto 93%, whereas private equity firm KKR, Infosys co-founder Nandan

Nilekani and Rakesh Jhunjhunwala’s Rare Enterprises make it to the list of

major shareholders with 3.43%, 1.77% and 0.24% equity stakes respectively.

Stakeholders: CCD’s parent company

Coffee Day Enterprises Limited (CDEL) is held by V G Siddarth-led promoter

group upto 93%, whereas private equity firm KKR, Infosys co-founder Nandan

Nilekani and Rakesh Jhunjhunwala’s Rare Enterprises make it to the list of

major shareholders with 3.43%, 1.77% and 0.24% equity stakes respectively.

ii.

Businesses: CDEL classify

themselves into mainly food service market, as their primary business is into

coffee products. In addition to having the largest chain of cafés in India,

CDEL also operates in procuring, processing and roasting of coffee beans and

retailing coffee products across various formats. Their diversification into

non-coffee businesses include technology park development, logistics solutions,

financial services, Resorts & Hospitality and ownership stakes in IT-ITES

companies like MindTree.

Businesses: CDEL classify

themselves into mainly food service market, as their primary business is into

coffee products. In addition to having the largest chain of cafés in India,

CDEL also operates in procuring, processing and roasting of coffee beans and

retailing coffee products across various formats. Their diversification into

non-coffee businesses include technology park development, logistics solutions,

financial services, Resorts & Hospitality and ownership stakes in IT-ITES

companies like MindTree.

iii.

Environment: Their claims about

the growth in coffee vending business gets justified with the changing

consumption pattern of northern and western Indian tea drinking population also

preferring to coffee consumption. Added by strong economic and demographic

aggregates like increasing percapita income, rising urbanisation, discretionary

spending, out-of-home food consumption trends, corporatisation etc., coffee

outlets today are in demand more than ever.

Environment: Their claims about

the growth in coffee vending business gets justified with the changing

consumption pattern of northern and western Indian tea drinking population also

preferring to coffee consumption. Added by strong economic and demographic

aggregates like increasing percapita income, rising urbanisation, discretionary

spending, out-of-home food consumption trends, corporatisation etc., coffee

outlets today are in demand more than ever.

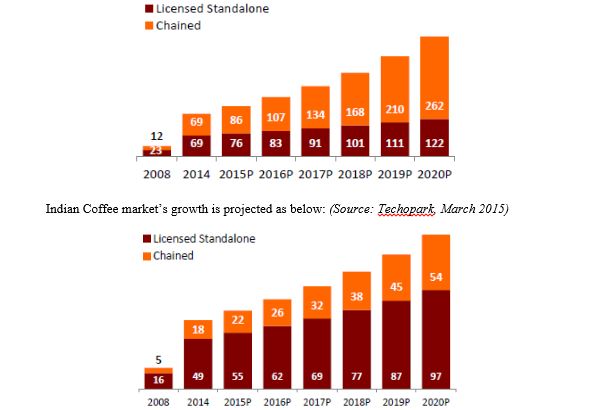

Indian QSR (Quick Service

Restaurants) market is expected to grow exponentially in the coming years. The

same (in Rs. Billion) is shown in the below graph. (Source: Techopark, March 2015)

Restaurants) market is expected to grow exponentially in the coming years. The

same (in Rs. Billion) is shown in the below graph. (Source: Techopark, March 2015)

iv.

Strengths: CDEL’s strengths are

strong home-grown brand, first-mover advantage, substantial market presence,

established network of franchises and dealers, multiple consumption points,

disorganised competition, scalability of the business, diversified businesses

focusing in India growth story and professional management.

Strengths: CDEL’s strengths are

strong home-grown brand, first-mover advantage, substantial market presence,

established network of franchises and dealers, multiple consumption points,

disorganised competition, scalability of the business, diversified businesses

focusing in India growth story and professional management.

v.

Strategic

View:

Currently, CDEL’s strategic outlook is to further deepen the existing chain of

cafés; increase café revenues by generating higher footfalls and driving

increased consumption; leverage brand equity of “Coffee Day” and “Café Coffee

Day”; constantly augur product range; and also develop non-coffee business.

Strategic

View:

Currently, CDEL’s strategic outlook is to further deepen the existing chain of

cafés; increase café revenues by generating higher footfalls and driving

increased consumption; leverage brand equity of “Coffee Day” and “Café Coffee

Day”; constantly augur product range; and also develop non-coffee business.

vi.

Financials: A simplified set of

consolidated financial statements for the previous five years were also

prepared like this:

Financials: A simplified set of

consolidated financial statements for the previous five years were also

prepared like this:

Consolidated Multi-Step Income Statement (Simplified) | |||||

Rs. in millions | |||||

Particulars | For the year ended 31st March | ||||

2011 | 2012 | 2013 | 2014 | 2015 | |

Revenue from Operations | 10244.04 | 15652.79 | 20995.60 | 22870.08 | 24793.55 |

Other Income | 725.15 | 685.92 | 495.84 | 657.63 | 693.60 |

Total Income | 10969.19 | 16338.71 | 21491.44 | 23527.71 | 25487.15 |

Cost of Goods Sold | 6727.64 | 7075.02 | 7205.34 | 7076.89 | 7751.94 |

Other Expenses | 1994.49 | 2150.65 | 2355.52 | 2570.32 | 2983.10 |

EBITDA | 2247.06 | 7113.04 | 11930.58 | 13880.50 | 14752.11 |

Depreciation | 792.45 | 935.69 | 1208.55 | 1540.76 | 1579.54 |

EBIT | 1454.61 | 6177.35 | 10722.03 | 12339.74 | 13172.57 |

Finance Costs | 464.56 | 431.90 | 399.80 | 449.40 | 554.98 |

EBT | 990.05 | 5745.45 | 10322.23 | 11890.34 | 12617.59 |

Tax Expenses | 101.18 | 104.78 | 93.55 | -1.37 | 44.46 |

EAT | 888.87 | 5640.67 | 10228.68 | 11891.71 | 12573.13 |

Extracts of Consolidated Balance Sheet | |||||

Rs. in millions | |||||

Particulars | For the year ended 31st March | ||||

2011 | 2012 | 2013 | 2014 | 2015 | |

Non-Current Assets | 7384.3 | 9302.07 | 10700.71 | 11251.42 | 10794.61 |

Shareholders’ Funds | 7566.96 | 7369.69 | 7344.04 | 7281.88 | 7693.05 |

Interest-bearing Non-Current Borrowings | 4355.66 | 4226.63 | 3713.46 | 3937.66 | 2844.03 |

Current Assets | 7627.30 | 5860.35 | 4172.2 | 3984.27 | 4546.98 |

Current Liabilities | 2735.78 | 3076.19 | 3146.95 | 3292.07 | 4092.01 |

Total Assets | 15011.60 | 15162.42 | 14872.19 | 15235.69 | 15341.59 |

Extracts of Cash Flow Statement | |||||

Rs. in millions | |||||

Particulars | For the year ended 31st March | ||||

2011 | 2012 | 2013 | 2014 | 2015 | |

Cash Flows from Operating Activities | 103.78 | 1520.04 | 1600.01 | 2304.60 | 3131.45 |

Cash Flows from Investing Activities | (2121.22) | (54.01) | (1078.10) | (1492.73) | (1147.97) |

Cash Flows from Financing Activities | 2646.03 | (611.97) | (852.16) | (803.87) | (1354.25) |

Purchase of Fixed Assets | (2005.80) | (2689.87) | (2452.10) | (1650.63) | (1460.67) |

vii.

IPO: The current issue

was to raise Rs. 11500 million with a price band of Rs. 316 to Rs. 328 per

share using book building process. Currently, the number of shares held by

owners is 170,940,744 with a face value of Rs. 10

IPO: The current issue

was to raise Rs. 11500 million with a price band of Rs. 316 to Rs. 328 per

share using book building process. Currently, the number of shares held by

owners is 170,940,744 with a face value of Rs. 10

The issue proceeds are

planned to be utilised towards repaying of existing debt to the tune of Rs.

6328 million (in FY16); financing for expansion of coffee business to the tune

of Rs. 2875.10 million (in FY16 – Rs. 1241.08 million; in FY17 – Rs. 1634.02

million) and rest to be used for general corporate purposes (evenly in the

coming two years)

planned to be utilised towards repaying of existing debt to the tune of Rs.

6328 million (in FY16); financing for expansion of coffee business to the tune

of Rs. 2875.10 million (in FY16 – Rs. 1241.08 million; in FY17 – Rs. 1634.02

million) and rest to be used for general corporate purposes (evenly in the

coming two years)

viii.

Market

& Competition:

Key players in the coffee outlets include Starbucks, Dunkin, CCD, Barista, Cost

Coffee and other minor operators. Their respective market shares are given in

the below table:

Market

& Competition:

Key players in the coffee outlets include Starbucks, Dunkin, CCD, Barista, Cost

Coffee and other minor operators. Their respective market shares are given in

the below table:

CDEL’s competitors include the

coffee outlets businesses as above; QSR operators such as McDonalds (WestLife),

Dominos (Jubiliant Foodworks) and KFC, Pizza Hut (YUM); food and grocery

businesses Nestle and HUL.

coffee outlets businesses as above; QSR operators such as McDonalds (WestLife),

Dominos (Jubiliant Foodworks) and KFC, Pizza Hut (YUM); food and grocery

businesses Nestle and HUL.

Swarup

uses Enterprise

DCF approach to arrive at the valuation. He decided to use some

modifications in the process, as he normally does and calls it Midas Touch of Swarup..!!:

uses Enterprise

DCF approach to arrive at the valuation. He decided to use some

modifications in the process, as he normally does and calls it Midas Touch of Swarup..!!:

ü He has decided to use

CAPM approach to compute cost of capital. Considering that this company do not

have historical data of prices, he wonders how to compute the beta. He has

anyways collected below information relating to industry players (those which

are listed):

CAPM approach to compute cost of capital. Considering that this company do not

have historical data of prices, he wonders how to compute the beta. He has

anyways collected below information relating to industry players (those which

are listed):

Jubiliant Foodworks | Nestle India | HUL | |

Beta | 0.14 | 0.62 | 0.11 |

Debt Equity Ratio | 0 | 0.37 | 0 |

Risk-Free Rate = 7.20% (RBI 10-year GOI yield) | |||

Nifty Monthly Returns annualised for the period 2011-2015 = 14.2% | |||

ü The marginal tax rate

for the corporate is 30%, and Swarup prefers to use this, instead of effective

tax rate, which is negative in many years for CDEL

for the corporate is 30%, and Swarup prefers to use this, instead of effective

tax rate, which is negative in many years for CDEL

ü He also wants use a

growth rate estimate as below. These rates are based on his discussions with

few of his friends in the equity research industry and also few industry

experts he keeps interacting on social networking platforms: From 2016 to 2025 – 17% p.a; After 2025 – 3.50% p.a infinitely. He

consciously avoids using the sustainable growth rate as this is the case of

IPO, which is expected to be a turnaround event and company’s prospects will be

way different from its past.

growth rate estimate as below. These rates are based on his discussions with

few of his friends in the equity research industry and also few industry

experts he keeps interacting on social networking platforms: From 2016 to 2025 – 17% p.a; After 2025 – 3.50% p.a infinitely. He

consciously avoids using the sustainable growth rate as this is the case of

IPO, which is expected to be a turnaround event and company’s prospects will be

way different from its past.

ü He wants to assign

weights to cash flows of last five years as below, for forecasting purposes, so

that he is giving higher importance to latest cash flows:

weights to cash flows of last five years as below, for forecasting purposes, so

that he is giving higher importance to latest cash flows:

2011 | 2012 | 2013 | 2014 | 2015 | |

Weights | 0.10 | 0.10 | 0.20 | 0.30 | 0.30 |

ü He decides to compute

FCFF first and then reduce the debt component to arrive at FCF for equity

shareholders.

FCFF first and then reduce the debt component to arrive at FCF for equity

shareholders.

ü Swarup also wants to

conduct a sensitivity analysis using Monte-Carlo simulation for changes in

above growth rates.

conduct a sensitivity analysis using Monte-Carlo simulation for changes in

above growth rates.

Questions:

(1)

Discuss

the possible valuation biases Swarup is exposed to in valuing CDEL.

Discuss

the possible valuation biases Swarup is exposed to in valuing CDEL.

(2)

How

do you compute the beta for an unlisted company?

How

do you compute the beta for an unlisted company?

(3)

Compute

the post-issue cost of capital for CDEL.

Compute

the post-issue cost of capital for CDEL.

(4)

Do

you agree with Swarup that sustainable growth rate of past cannot be applied in

the case of valuing an IPO?

Do

you agree with Swarup that sustainable growth rate of past cannot be applied in

the case of valuing an IPO?

(5)

What

will be the projected FCFF for CDEL for the next 10 years and the terminal

FCFF?

What

will be the projected FCFF for CDEL for the next 10 years and the terminal

FCFF?

(6)

What

will be post-issue intrinsic value per share of CDEL?

What

will be post-issue intrinsic value per share of CDEL?

(7)

Conduct

a simulation using MS-Excel for varying rates of growth of next 10 years from

12% to 24% (changing interval of 1%) and terminal growth rate from 0% to 6%

(changing interval of 0.50%). What will be the expected post-issue intrinsic

value per share of CDEL

Conduct

a simulation using MS-Excel for varying rates of growth of next 10 years from

12% to 24% (changing interval of 1%) and terminal growth rate from 0% to 6%

(changing interval of 0.50%). What will be the expected post-issue intrinsic

value per share of CDEL

(8)

Discuss

the areas of subjectivity involved in the entire CDEL valuation exercise of

Swarup and what other alternatives were skipped in the process.

Discuss

the areas of subjectivity involved in the entire CDEL valuation exercise of

Swarup and what other alternatives were skipped in the process.

~~ End of Case ~~

INSTRUCTOR REFERENCES:

I.

What courses are

intended to be using this case?

What courses are

intended to be using this case?

The case can be used

as part finance courses like Financial Management, Security Analysis, M&A,

Investment Banking, Corporate Valuation, Financial

Modeling/Analytics/Engineering

as part finance courses like Financial Management, Security Analysis, M&A,

Investment Banking, Corporate Valuation, Financial

Modeling/Analytics/Engineering

II.

What

concepts/models/theories can be explained through this case?

What

concepts/models/theories can be explained through this case?

This case can be used

to demonstrate the below concepts/theories/models/applications:

to demonstrate the below concepts/theories/models/applications:

i)

Corporate

Objective – Shareholder Wealth maximisation to Intrinsic Value Maximisation

Corporate

Objective – Shareholder Wealth maximisation to Intrinsic Value Maximisation

ii)

Concept

of Intrinsic Value

Concept

of Intrinsic Value

iii)

Valuation

biases, subjectivity and Challenges

Valuation

biases, subjectivity and Challenges

iv)

Accounting

Profit Vs. FCFF, FCFE

Accounting

Profit Vs. FCFF, FCFE

v)

Cost

of Capital (WACC); CAPM; Cost of Equity for unlisted company

Cost

of Capital (WACC); CAPM; Cost of Equity for unlisted company

vi)

IPO

Process

IPO

Process

vii)

Enterprise

DCF Technique

Enterprise

DCF Technique

viii)

Financial

Modelling using MS-Excel for corporate valuation

Financial

Modelling using MS-Excel for corporate valuation

ix)

Sensitivity

Analysis using Monte-Carlo Simulation using MS-Excel

Sensitivity

Analysis using Monte-Carlo Simulation using MS-Excel

III.

What main

issue/problem is addressed in the case?

What main

issue/problem is addressed in the case?

The case addresses the

problem of valuing an unlisted company during its IPO that is already a

household name, and hence, has ample scope for pre-valuation bias

problem of valuing an unlisted company during its IPO that is already a

household name, and hence, has ample scope for pre-valuation bias

IV.

Teaching Notes:

Teaching Notes:

1)

The

anchor books for the above case would be,

The

anchor books for the above case would be,

ü

“Damodaran

on Valuation: Security Analysis for Investment and Corporate Finance, 2nd

Edition” (Author: Aswath

Damodaran) by Wiley Publishing

“Damodaran

on Valuation: Security Analysis for Investment and Corporate Finance, 2nd

Edition” (Author: Aswath

Damodaran) by Wiley Publishing

ü

“Corporate

Valuation and value Creation” (Author:

Prasanna Chandra) by McGraw Hill

“Corporate

Valuation and value Creation” (Author:

Prasanna Chandra) by McGraw Hill

ü

“Financial Management: A Step-by-Step

Approach” (Author: N R Parasuraman)

by Cengage Learning

“Financial Management: A Step-by-Step

Approach” (Author: N R Parasuraman)

by Cengage Learning

2)

This

case can best be solved using MS-Excel.

Student should be comfortable in entering formulas, using functions and using

What-if Analysis feature in MS-Excel.

This

case can best be solved using MS-Excel.

Student should be comfortable in entering formulas, using functions and using

What-if Analysis feature in MS-Excel.

3)

A

total for 4 sessions (approximately

5 hours of classroom discussion with demonstration is required). Ideal if the

students are grouped into groups of 3-4 members in each.

A

total for 4 sessions (approximately

5 hours of classroom discussion with demonstration is required). Ideal if the

students are grouped into groups of 3-4 members in each.

4) Possible

Approaches for solving the key issues: (Explained Question-wise)

Approaches for solving the key issues: (Explained Question-wise)

Question-(1)

: Discuss the possible valuation biases Swarup is exposed to in valuing CDEL.

: Discuss the possible valuation biases Swarup is exposed to in valuing CDEL.

As Swarup is already having positive impression of

CCD (as a customer), he might be biased while using some inputs, like, the

growth rate, overlooking of past performance etc. (Input Bias); He may also revisit his assumptions after valuation if

his value differs from the Band Price of Rs. 316 to Rs. 328 (Post-Valuation Tinkering Bias); He may

also dedicate the distance between his value and the price band to qualitative

factors, like strategic consideration etc.(qualitative

factor bias). (Refer Damodaran –

Chapter-1)

CCD (as a customer), he might be biased while using some inputs, like, the

growth rate, overlooking of past performance etc. (Input Bias); He may also revisit his assumptions after valuation if

his value differs from the Band Price of Rs. 316 to Rs. 328 (Post-Valuation Tinkering Bias); He may

also dedicate the distance between his value and the price band to qualitative

factors, like strategic consideration etc.(qualitative

factor bias). (Refer Damodaran –

Chapter-1)

Question-(2)

: How do you compute the beta for an unlisted company?

: How do you compute the beta for an unlisted company?

Step-1: Compute the asset betas of listed

competitors – HUL, Nestle & JFW

competitors – HUL, Nestle & JFW

Step-2: Compute the equity betas using the above

asset betas.

asset betas.

Step-3: Compute the average equity beta

Step-4: Compute the equity beta of CDEL using

proposed capital structure

proposed capital structure

(Refer Prasanna

Chandra – Chapter-3)

Chandra – Chapter-3)

Question-(3)

Compute the post-issue cost of capital for CDEL

Compute the post-issue cost of capital for CDEL

Compute WACC using post-issue weights

(Refer Prasanna

Chandra – Chapter-3)

Chandra – Chapter-3)

Question-(4)

Do you agree with Swarup that sustainable growth rate of past cannot be

applied in the case of valuing an IPO?

Do you agree with Swarup that sustainable growth rate of past cannot be

applied in the case of valuing an IPO?

Yes. CDEL has incurred losses in two out of last 4

years. The purpose of IPO is primarily to clear the debt. The financial performances

will turnaround once the debt is cleared and planned expansion take place. This

will not be reflected if we consider sustainable growth rate (ROE X Retention

Ratio) of past years.

years. The purpose of IPO is primarily to clear the debt. The financial performances

will turnaround once the debt is cleared and planned expansion take place. This

will not be reflected if we consider sustainable growth rate (ROE X Retention

Ratio) of past years.

(Refer Damodaran –

Chapter-3 & 4)

Chapter-3 & 4)

Question-(5) What will

be the projected FCFF for CDEL for the next 10 years and the

terminal FCFF?; Question-(6) What will

be post-issue intrinsic value per share of CDEL?

be the projected FCFF for CDEL for the next 10 years and the

terminal FCFF?; Question-(6) What will

be post-issue intrinsic value per share of CDEL?

Step-1: Prepare

projected income statements for next 10 years, applying the growth rate given

in the case on the sales numbers. Using common size approach, project the other

numbers.

projected income statements for next 10 years, applying the growth rate given

in the case on the sales numbers. Using common size approach, project the other

numbers.

Step-2: Compute

projected FCFF for next 10 years

projected FCFF for next 10 years

Step-3: Compute the

terminal cash flow using Gordon’s model and compute the present value

terminal cash flow using Gordon’s model and compute the present value

Step-4: Compute the

present value of all cash flows = FCFF or Value of the Firm

present value of all cash flows = FCFF or Value of the Firm

Step-5: Deduct the

debt component = FCFE or Value of Firm for Equity Shareholders

debt component = FCFE or Value of Firm for Equity Shareholders

Step-6: Divide FCFE by

number of equity shares post-issue = Intrinsic Value per Share

number of equity shares post-issue = Intrinsic Value per Share

(Refer

Damodaran – Chapters – 4,5 & 6; Prasanna Chandra – Chapter -2)

Damodaran – Chapters – 4,5 & 6; Prasanna Chandra – Chapter -2)

Question-(7) Conduct a

simulation using MS-Excel for varying rates of growth of next 10 years from 12%

to 24% (changing interval of 1%) and terminal growth rate from 0% to 6%

(changing interval of 0.50%). What will be the expected post-issue intrinsic

value per share of CDEL

simulation using MS-Excel for varying rates of growth of next 10 years from 12%

to 24% (changing interval of 1%) and terminal growth rate from 0% to 6%

(changing interval of 0.50%). What will be the expected post-issue intrinsic

value per share of CDEL

Use

MS-Excel>>Data>>What-if Analysis>>Scenario Manager

MS-Excel>>Data>>What-if Analysis>>Scenario Manager

Use

MS-Excel>>Data Analysis>>Random Number Generation>>Conduct

Simulation

MS-Excel>>Data Analysis>>Random Number Generation>>Conduct

Simulation

(Refer

Parasuraman – Chapter-17)

Parasuraman – Chapter-17)

Question-(8) Discuss

the areas of subjectivity involved in the entire CDEL valuation exercise of

Swarup and what other alternatives were skipped in the process

the areas of subjectivity involved in the entire CDEL valuation exercise of

Swarup and what other alternatives were skipped in the process

Areas | Swarup’s Action | Possible Alternatives |

Growth Rate | Expert Opinion | Regress with Economic Numbers Sustainable Growth Rate (ROE X RR) |

Competitors | HUL, Nestle, JFW | Other Hotel Stocks |

Forecast Period | 10 years | Can consider the Business Cycle and Decide |

Risk-free rate | 7.20% | Could’ve adjusted for long-term interest rate expectation |

Cost of equity | CAPM | Dividend Discount Model; Bon-Yield Plus Risk Premium; APT; FF Five Factor Model |

Tax Rate | Marginal Tax Rate | Effective Tax Rate |

Capital Structure Weights | Current | Long-term Target Capital Structure |