Abstract: The rapid growth of Buy Now, Pay Later (BNPL) services has significantly transformed digital payment behaviour by allowing consumers to defer payments while making immediate purchases. While BNPL is promoted as a convenient and flexible payment option, concerns have been raised about its behavioural implications, particularly in shaping consumers’ perception of affordability and debt. This study examines whether BNPL usage creates a perceived sense of affordability and leads to an underestimation of total debt among digital payment users. It further explores the relationship between BNPL usage and impulse buying behaviour, budgeting practices, and awareness of repayment terms.The study adopts a behavioural perspective to analyse how BNPL influences purchase decision-making at the point of sale and compares the level of debt awareness between BNPL users and non-BNPL users. By assessing consumers’ budgeting behaviour, impulse purchasing tendencies, and understanding of repayment obligations, the research provides insights into the financial risks associated with deferred payment mechanisms. The findings of the study aim to contribute to existing literature on digital finance and consumer behaviour while offering practical implications for policymakers, financial service providers, and consumers to promote responsible usage of BNPL services. Overall, this study seeks to highlight the need for greater financial awareness and responsible usage of BNPL services in an increasingly digital economy.

Key Words: Buy Now Pay Later (BNPL), Illusion of Affordability, Underestimation of Debt, Consumer Behavior, Digital Payments

1. Introduction:

The digitalization of financial services has reshaped consumer payment behaviour, with digital payment platforms becoming an integral part of everyday transactions. Among recent innovations, Buy Now, Pay Later (BNPL) services have gained widespread popularity, especially among young and digitally active consumers. These services allow individuals to purchase goods immediately while deferring payment to a later date or splitting it into instalments, often with minimal upfront costs. The ease of access and seamless integration of BNPL into online and offline checkout processes have made it an attractive alternative to traditional payment methods such as credit cards and cash.

Despite their increasing adoption, BNPL services present notable behavioural and financial challenges. By postponing payment obligations, these services may weaken the perceived cost of spending, encouraging consumers to exceed their actual financial capacity. The separation between purchase and payment can distort affordability perceptions, leading individuals to overlook their cumulative financial commitments.

An additional concern is the impact of BNPL on impulsive purchasing and financial planning. The availability of deferred payment options at the point of purchase may reduce self-control, resulting in unplanned spending and weaker budgeting discipline. Moreover, limited awareness or understanding of repayment schedules, penalties, and late fees can further exacerbate debt accumulation, especially when multiple BNPL transactions are used simultaneously across platforms.

In this context, the present study seeks to examine the behavioural implications of Buy Now, Pay Later services among digital payment consumers. Specifically, it focuses on understanding whether BNPL creates an illusion of affordability, contributes to the underestimation of debt, influences purchase decision-making, and affects budgeting and impulse buying behaviour2. By comparing BNPL users with non-BNPL users, the study aims to provide a comprehensive assessment of debt awareness and financial decision-making in the evolving digital payment landscape.

Literature Review

Prior research on digital payment systems indicates that deferred payment options can alter consumer spending behavior by reducing the immediate pain of payment. Studies on Buy Now, Pay Later (BNPL) services suggest that such mechanisms may create an illusion of affordability, encouraging higher spending and impulsive purchases. Behavioral finance literature also highlights that payment deferral can lead consumers to underestimate their total debt obligations. However, limited empirical research examines these effects in the context of digital payment consumers, highlighting the need for further study.

As per the study of Nusir et al. (2026)[ https://www.mdpi.com/0718-1876/21/2/43], “The Psychology of BNPL: A Systematic Review of Impulsive Buying and Post-Purchase Regret (2018–2025)”, synthesize existing empirical research on the behavioral and psychological effects of Buy Now, Pay Later services. The review identifies deferred payments, perceived affordability, and urgency cues as consistent predictors of impulsive purchasing and reduced payment salience. However, the authors highlight that most prior studies rely on proxy indicators such as financial distress and emotional discomfort rather than directly measuring post-purchase regret. The study emphasizes a significant theoretical and methodological gap in BNPL research and calls for future studies using validated regret measures, longitudinal designs, and ethically informed frameworks.

Simolinna, Karen (2025)[ https://aaltodoc.aalto.fi/server/api/core/bitstreams/69647745-d1ec-4344-91a4-43e10bd791b8/content] in their bachelor’s thesis “The Influence of Buy Now, Pay Later Services on Consumer Spending Behavior”, investigates how BNPL services affect consumer behavior and financial well-being, particularly among young adults. The study highlights that deferred and installment-based payment structures reduce the perceived burden of paying, thereby increasing impulsive purchasing tendencies. Findings further reveal that BNPL usage diminishes consumers’ perception of financial risk, often leading to debt accumulation, especially among individuals with lower financial literacy. The thesis contributes to existing literature by emphasizing how largely unregulated BNPL credit promotes short-term consumption while increasing long-term financial vulnerability.

In the research technical paper by Jose et al. (2025)[ https://ideas.repec.org/j/G41.html] titled “Buy Now, Spend More, Pay Later: Behavioural Mechanisms of Buy Now Pay Later Products”, investigated the behavioural effects of BNPL using an experimental study with a nationally representative sample in Ireland. The findings show that consumers spend on average 4.39% more when using BNPL compared to debit cards, highlighting the spending-enhancing nature of deferred payments. The study also demonstrates strong mental accounting and anticipatory effects, where perceived increases in available funds and expected future access to BNPL significantly raise discretionary spending. Despite improved risk comprehension through salient disclosures, BNPL usage and spending patterns remain largely unchanged, underscoring the need for stronger consumer protection measures and policy attention.

Ashby et al. (2025)6 in his study “The Influence of the Buy-Now-Pay-Later Payment Mode on Consumer Spending Decisions”, examine how BNPL affects consumer spending compared to other payment methods. Using transaction data and controlled experiments, the authors find that BNPL leads to higher spending even when compared to credit cards. The study shows that displaying installment prices (such as small per-payment amounts) lowers how expensive a purchase feels, which encourages consumers to spend more. It also finds that having more installments or a smaller first payment further increases BNPL-related spending, offering important insights for retailers and policymakers.

In the study “The Effects of Buy Now, Pay Later (BNPL) on Customers’ Online Purchase Behavior”, by Kumar, Salo, and Bezawada (2024)[ https://www.sciencedirect.com/science/article/pii/S0022435924000654] it is examined how BNPL adoption influences online spending using a synthetic difference-in-differences research design. The findings reveal that customers who adopt BNPL spend approximately 6.42% more online compared to those using traditional payment methods. The effect is particularly pronounced for low-ticket items and among younger, low-income consumers, as well as customers with high category experience and promotion sensitivity. The study contributes empirical evidence on how BNPL reshapes online purchasing patterns and offers strategic insights for retailers regarding targeted BNPL implementation.

According to the study by Syamsulang Hj. Sarifuddin (2024)[ https://ijsps.ism.gov.my/IJSPS/article/view/332], titled “Buy Now, Pay Later or Pain Later? A Qualitative Study on the Adoption of BNPL and Financial Risks among Generation Z Consumers in Klang Valley”, explores the psychological, social, and financial factors driving BNPL adoption among Generation Z consumers in Malaysia. The findings identify instant gratification and Fear of Missing Out (FOMO) as key psychological motivators, while peer influence and social media exposure significantly shape BNPL usage behavior. The study also reveals frequent financial consequences, including impulsive purchasing, repayment difficulties, and debt accumulation. Additionally, limited financial literacy and poor understanding of BNPL terms highlight the need for stronger regulatory frameworks and targeted consumer education initiatives.

Di Maggio, Williams, and Katz (2022)[ https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4198320] in his research, studied how Buy Now, Pay Later (BNPL) affects spending by analyzing real transaction data from U.S. consumers. They found that when people get access to BNPL, they spend more overall, especially on retail purchases. This increase happens even for consumers who are not short of money, showing that BNPL encourages extra spending rather than just shifting spending over time. The authors explain this using a “liquidity flypaper effect,” meaning the extra buying power from BNPL is quickly spent instead of being saved.

Another study by Rafidarma and Aprilianty (2022)[ https://www.studocu.vn/vn/document/truong-dai-hoc-tai-chinh-marketing/nghien-cuu-khoa-hoc/19336-1318-64894-2-10-20220901/116196416], titled “The Impact of Buy Now Pay Later Feature Towards Online Buying Decision in E-Commerce Indonesia”, examine how BNPL features affect online purchase decisions on major Indonesian e-commerce platforms. Using survey data from 240 BNPL users across Shopee, Tokopedia, and Lazada, the study finds that perceived usefulness and ease of use increase consumers’ intention to use BNPL. However, factors such as impulsive buying, materialism, and budget constraints were not found to significantly influence BNPL adoption. The results also show that a stronger intention to use BNPL positively affects online buying decisions, highlighting BNPL’s role in shaping e-commerce behaviour.

Research Gap

Although existing studies show that Buy Now, Pay Later (BNPL) services increase consumer spending, impulsive buying, and perceived affordability, most research primarily focuses on adoption patterns and spending outcomes rather than consumers’ internal perception of affordability and awareness of cumulative debt at the point of purchase. Prior studies frequently rely on proxy measures such as financial distress or regret instead of directly examining the illusion of affordability and underestimation of debt as behavioural constructs. Moreover, empirical comparisons between BNPL users and non-BNPL users with respect to debt awareness and budgeting behaviour remain limited, particularly among digital payment consumers. Consequently, there is a clear gap in integrated research that simultaneously examines affordability perception, debt underestimation, purchase decision-making, budgeting behaviour, and impulsive buying in the context of BNPL usage.

Research Questions

- Does the use of Buy Now, Pay Later (BNPL) services lead to an illusion of affordability and an underestimation of total debt among digital payment consumers?

- In what ways does BNPL usage affect consumers’ purchase decision-making at the point of sale?

- Is there a measurable difference in debt awareness between consumers who use BNPL services and those who do not?

- How does the use of BNPL influence consumers’ budgeting practices and impulsive buying behavior?

Objectives of the Study

- To examine whether the use of Buy Now Pay Later (BNPL) services create an illusion of affordability and leads to underestimation of debt among digital payment users.

- To examine how the use of BNPL influences consumers’ purchase decision-making at the point of sale.

- To compare the level of debt awareness between BNPL users and non-BNPL users.

- To assess the impact of BNPL usage on budgeting behaviour and impulsive purchasing decisions.

Research Methodology

This study adopts a quantitative research design to examine the behavioural implications of Buy Now, Pay Later (BNPL) services among digital payment consumers.

Sampling and Data Collection

Primary data was collected using a structured questionnaire administered through Google Forms. A non-probability convenience sampling technique was employed to select respondents based on accessibility and relevance to the study. A total of 101 valid responses were collected from digital payment users and used for analysis.

Questionnaire Design

The questionnaire was close-ended and structured, consisting of multiple-choice questions designed to capture respondents’ BNPL usage behaviour, perception of affordability, debt awareness, and purchase decision-making patterns.

Measurement and Scale

The study utilized ordinal and nominal scales for measurement. BNPL usage frequency was measured using an ordinal scale (Rarely = 1, Occasionally = 2, Frequently = 3), while awareness of total debt obligations was measured using a binary nominal scale (Yes = 1, No = 0). These measures facilitated statistical analysis such as correlation and Chi-square tests.

Validity of the Instrument

The questionnaire ensured content validity by being developed based on established concepts from behavioural finance and consumer behaviour literature. The items were aligned with the research objectives and reviewed for clarity, relevance, and consistency prior to data collection.

Data Collection Period

The data was collected over a period of 30 days, allowing adequate time to obtain responses from a diverse set of digital payment users.

Data Analysis

Buy Now, Pay Later (BNPL) has emerged as a widely adopted digital payment method that allows consumers to delay payments while completing transactions immediately. While this model enhances convenience, it also raises concerns regarding its influence on spending behaviour, financial awareness, and budgeting discipline. By reducing the immediate pain of payment, BNPL may encourage impulsive buying and weaken budgeting discipline. This study empirically examines how BNPL usage affects affordability perception, debt awareness, purchase decision-making, and budgeting behaviour among digital payment users.

Correlation Analysis Between BNPL Usage and Underestimation of Debt

This analysis examines the relationship between the frequency of Buy Now Pay Later (BNPL) usage and consumers’ tendency to underestimate their total outstanding debt. Pearson correlation analysis is employed to assess the strength and direction of the association between BNPL usage and debt awareness. The analysis helps determine whether increased reliance on BNPL services is linked to reduced recognition of cumulative financial obligations. The findings provide empirical evidence for evaluating the illusion of affordability associated with BNPL usage.

Table 1: Definition of Variables (X and Y)

| Symbol | Variable | Description | Measurement & Coding |

|---|---|---|---|

| X | BNPL Usage Frequency | Frequency with which respondents use BNPL services | Rarely = 1 Occasionally = 2 Frequently = 3 |

| Y | Underestimation of Debt (Debt Awareness) | Awareness of total outstanding financial obligations while using BNPL | Yes = 1 (Aware) No = 0 (Underestimates Debt) |

Source: Primary data collected through a structured questionnaire administered via Google Forms. A total of 101 valid responses were received from digital payment users and used for the purpose of data analysis.

Table 2: Distribution of Respondents Based on BNPL Usage Frequency (Variable X)

| Response Category | Code | Number of Respondents |

|---|---|---|

| Rarely | 1 | 86 |

| Occasionally | 2 | 10 |

| Frequently | 3 | 5 |

| Total | 101 |

Source: Primary data was gathered using an online questionnaire distributed through Google Forms. A total of 101 valid responses were received from digital payment users and used for the purpose of data analysis.

Table 3: Bifurcation of Respondents Based on Underestimation of Debt (Variable Y)

| Response Category | Code | Number of Respondents | Percentage (%) |

|---|---|---|---|

| Yes (Aware of Total Outstanding Debt) | 1 | 60 | 59.4 |

| No (Underestimates Total Debt) | 0 | 41 | 40.6 |

| Total | 101 | 100.0 |

Source: Data was collected through a structured online survey. A total of 101 valid responses were received from digital payment users.

Table 4: Descriptive Statistics for BNPL Usage Frequency and Underestimation of Debt

| Variable | N | Mean | Standard Deviation |

|---|---|---|---|

| BNPL Usage Frequency (X) | 101 | 1.20 | 0.53 |

| Underestimation of Debt (Y) | 101 | 0.41 | 0.49 |

Source: Responses were obtained using a digital questionnaire. A total of 101 valid responses were received from digital payment users and used for the purpose of data analysis.

Basis for Correlation

From Tables 1–4:

- Variable X: BNPL Usage Frequency

(Rarely = 1, Occasionally = 2, Frequently = 3) - Variable Y: Underestimation of Debt

(Yes = 1, No = 0) - Number of respondents = 101

- Mean of X = 1.20

- Mean of Y = 0.41

The correlation value was computed using the CORREL function in MS Excel based on the coded responses.

Table 5: Correlation between BNPL Usage (X) and Underestimation of Debt (Y)

| Variables | Correlation Value (r) |

|---|---|

| BNPL Usage Frequency & Underestimation of Debt | 0.26 |

Source: Calculation based on primary data using MS Excel (N = 101)

Interpretation

The correlation coefficient of r = 0.26 indicates a positive relationship between BNPL usage and underestimation of debt. This shows that respondents who use BNPL services more frequently tend to be less aware of their total outstanding financial obligations. Although the relationship is weak, it suggests that increased reliance on BNPL is associated with a greater tendency to underestimate debt. The result therefore supports Objective 1 and confirms that BNPL usage contributes to an illusion of affordability among digital payment users.

Result:

The study finds a positive correlation (r = 0.26) between BNPL usage and underestimation of debt, indicating that higher BNPL usage is linked with lower debt awareness.

Analysis of the Influence of BNPL on Consumers’ Purchase Decision-Making at the Point of Sale

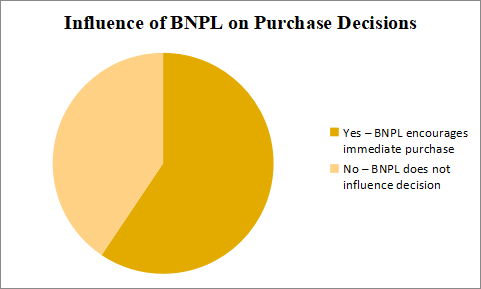

Table 6: Influence of BNPL on Purchase Decisions at the Point of Sale

| Response | Number of Respondents | Percentage (%) |

|---|---|---|

| Yes – BNPL encourages immediate purchase | 60 | 59.4 |

| No – BNPL does not influence decision | 41 | 40.6 |

| Total | 101 | 100 |

Source: Primary data was gathered using an online questionnaire distributed through Google Forms. A total of 101 valid responses were received from digital payment users and used for the purpose of data analysis.

Figure 1: Impact of BNPL on Immediate Purchase Decisions

Source: Primary data collected through a structured questionnaire administered via Google Forms. A total of 101 valid responses were received from digital payment users and used for the purpose of data analysis.

Interpretation

The above table and pie chart present the influence of BNPL on consumers’ purchase decisions at the point of sale. Out of 101 respondents, 60 respondents (59.4%) agreed that BNPL encourages them to make purchases that they would otherwise postpone, while 41 respondents (40.6%) stated that BNPL does not influence their decision.

These findings suggest that consumers’ purchasing decisions are significantly influenced by the availability of deferred payment options.The facility of deferred payment appears to reduce the immediate financial burden and makes products seem more affordable, thereby encouraging instant buying decisions. The results align with the study’s objective and highlight the behavioural impact of BNPL on consumer decision-making.

Result

Majority of respondents (59.4%) reported that BNPL availability encourages immediate purchases, confirming that BNPL significantly influences consumer decision-making at the point of sale.

Analysis of the Association between BNPL Usage and Budgeting Behaviour and Impulsive Purchasing Decisions

Table 7: BNPL Usage and Budgeting Behaviour & Impulsive Purchasing

| BNPL Usage | Disrupts Budgeting & Increases Impulsive Buying (Yes) | No Significant Impact (No) | Total |

|---|---|---|---|

| Yes | 40 | 22 | 62 |

| No | 23 | 16 | 39 |

| Total | 63 | 38 | 101 |

Source: Primary data was gathered using an online questionnaire distributed through Google Forms

Table Interpretation

The table shows that a majority of BNPL users (40 out of 62) reported that BNPL usage disrupted their budgeting behaviour and increased impulsive purchases. In comparison, non-BNPL users reported a relatively lower impact. This distribution supports the conclusion that BNPL usage is associated with changes in budgeting discipline and impulse buying tendencies, making it suitable for Chi-Square analysis.

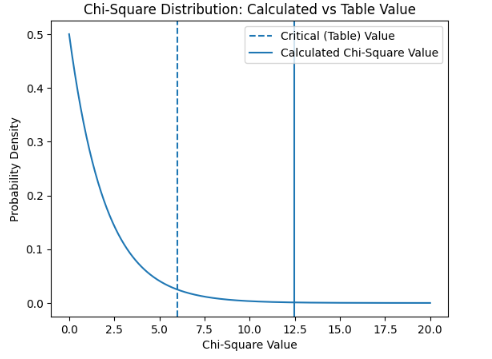

Chi-Square Test

Figure 2: Chi-Square distribution showing association between BNPL usage and budgeting behaviour

Source: Computed by the authors based on primary survey data

The above chart represents the Chi-Square distribution comparing the calculated Chi-Square value with the critical (table) value at a 5% level of significance.

From the chart, it is clearly observed that the calculated Chi-Square value lies to the right of the critical Chi-Square (table) value. This indicates that the calculated value exceeds the critical value required for acceptance of the null hypothesis.

Statistical Inference

Since the calculated Chi-Square value is greater than the table value, the null hypothesis is rejected and the alternative hypothesis is accepted. This confirms that there exists a statistically significant association between BNPL usage and budgeting behaviour as well as impulsive purchasing decisions.

Interpretation in the Context of the Study

The rejection of the null hypothesis implies that BNPL usage significantly influences consumers’ financial behaviour. The deferred payment facility reduces the immediate financial outflow at the point of sale, thereby encouraging consumers to make impulsive purchase decisions and deviate from planned budgets. This behavioural shift suggests that BNPL services alter traditional spending discipline by separating purchase decisions from immediate payment responsibility.

Result:

Based on the Chi-Square test results, it can be concluded that BNPL usage has a significant impact on budgeting behaviour and impulsive purchasing decisions among consumers. Even though users may possess awareness regarding repayment obligations, the convenience and perceived affordability associated with BNPL services increase the likelihood of unplanned spending.

Analysis of the Impact of BNPL Usage on Immediate Purchase Decisions

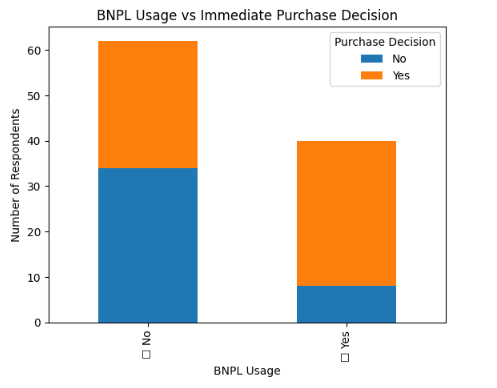

Table 8: BNPL Usage vs Immediate Purchase Decision

| BNPL Usage | Immediate Purchase – Yes | Immediate Purchase – No | Total |

|---|---|---|---|

| Yes | 32 | 8 | 40 |

| No | 28 | 34 | 62 |

| Total | 60 | 42 | 102 |

*Total variation may occur due to rounding or non-response in survey data.

Source: Primary data collected through a structured questionnaire administered via Google Forms

Table Interpretation

The table indicates that BNPL users are more likely to make immediate purchase decisions, with 32 respondents agreeing that BNPL encouraged instant buying. On the other hand, a majority of non-BNPL users (34 respondents) reported that BNPL did not influence their purchase decisions. This clearly demonstrates the role of BNPL in accelerating purchase decisions at the point of sale.

The above stacked bar chart illustrates the relationship between BNPL usage and immediate purchase decisions among respondents. The chart compares BNPL users and non-BNPL users based on whether BNPL encouraged them to make an immediate purchase at the point of sale.

Figure 3: BNPL Usage vs Immediate Purchase Decision

Source: Computed by the authors based on primary survey data

Interpretation

From the chart, it is evident that a higher number of respondents who use BNPL services reported “Yes” to making immediate purchase decisions compared to non-BNPL users. Among BNPL users, the proportion of respondents who indicated that BNPL encouraged instant purchasing is significantly larger than those who reported no influence.

In contrast, among non-BNPL users, the majority of respondents fall under the “No” category, indicating that the absence of BNPL facilities reduces the likelihood of making instant or unplanned purchases.

Behavioural Insight

The findings suggest that BNPL services reduce the psychological barrier associated with immediate payment, thereby encouraging consumers to complete purchases without prolonged evaluation or budget consideration. The deferred payment mechanism makes the transaction appear more affordable at the point of sale, which increases the tendency toward impulsive buying behaviour.

Result:

Based on the graphical analysis, it can be concluded that BNPL usage has a significant impact on immediate purchase decisions. Consumers who have access to BNPL are more likely to make instant buying decisions compared to non-BNPL users. This supports the objective that BNPL influences consumer behaviour by accelerating purchase decisions and weakening traditional spending restraint.

Findings

- The correlation analysis showed a positive relationship (r = 0.26) between BNPL usage frequency and underestimation of debt, indicating that higher BNPL usage is associated with lower awareness of total outstanding financial obligations.

- A majority of respondents (59.4%) reported that the availability of BNPL encourages them to make purchases they would otherwise postpone, demonstrating its strong influence on purchase decisions at the point of sale.

- Among BNPL users, a larger proportion reported disruptions in budgeting behaviour and increased impulsive spending compared to non-BNPL users, suggesting that BNPL weakens financial discipline.

- The Chi-Square test confirmed a statistically significant association between BNPL usage and budgeting behaviour as well as impulsive purchasing decisions, leading to the rejection of the null hypothesis.

- BNPL users showed a higher tendency to make immediate purchase decisions compared to non-users, indicating that deferred payment options accelerate buying behaviour.

- Overall, the findings suggest that BNPL reduces the psychological impact of immediate payment, creating an illusion of affordability that encourages impulsive purchases and weakens awareness of total debt.

Suggestions

- BNPL providers and financial institutions should display the total outstanding amount across all active BNPL plans so that users clearly understand their overall debt and avoid underestimation.

- Applications should provide real-time spending alerts and repayment reminders when users cross spending limits or have multiple active BNPL plans, helping them maintain better financial control.

- BNPL platforms should include simple budgeting tools that show how each installment affects monthly expenses, encouraging more disciplined spending and reducing impulsive purchases.

- Providers should conduct stricter eligibility checks and assess the repayment capacity of users, especially frequent users, to prevent excessive borrowing and debt accumulation.

- Banks, fintech companies, and regulators should promote financial literacy programs that educate consumers about the risks of deferred payments, interest charges, penalties, and multiple credit commitments.

Conclusion

The present study examined the behavioural implications of Buy Now, Pay Later (BNPL) services with a focus on the illusion of affordability, underestimation of debt, purchase decision-making, and budgeting behaviour among digital payment consumers[ Gathergood, J., & Weber, J. (2017). Financial literacy, present bias and alternative mortgage products. Journal of Banking & Finance, 78, 58–83.]. The findings indicate that BNPL usage is positively associated with the underestimation of total outstanding debt. Although the correlation observed was weak, it still suggests that increased reliance on BNPL services may reduce consumers’ awareness of their cumulative financial obligations. This supports the behavioural finance perspective that separating the act of purchase from the act of payment can distort affordability perceptions.

The analysis also revealed that a majority of respondents reported that BNPL encourages immediate purchase decisions. The availability of deferred payment options at the point of sale reduces the psychological barrier of immediate payment, making products appear more affordable and encouraging unplanned spending. The comparative results between BNPL users and non-users further showed that individuals using BNPL are more likely to make instant buying decisions, confirming its influence on consumer decision-making behaviour.

In addition, the Chi-Square test established a statistically significant association between BNPL usage and changes in budgeting behaviour as well as impulsive purchasing tendencies. A larger proportion of BNPL users reported disruptions in budgeting discipline compared to non-users, indicating that deferred payment mechanisms may weaken financial planning and self-control. These findings collectively highlight that BNPL services, while convenient, can alter traditional spending behaviour by separating consumption from immediate financial consequences.

Overall, the study concludes that BNPL services tend to create a perceived sense of affordability, encourage impulsive purchasing, and reduce awareness of total financial obligations among users. While BNPL offers flexibility and convenience, its behavioural impact raises concerns about long-term financial discipline and debt management. The results emphasize the need for responsible BNPL usage, improved consumer awareness, and appropriate regulatory and financial literacy initiatives to ensure that the benefits of digital credit do not lead to unintended financial risks.

- https://www.mdpi.com/0718-1876/21/2/43

- https://aaltodoc.aalto.fi/server/api/core/bitstreams/69647745-d1ec-4344-91a4-43e10bd791b8/content

- https://ideas.repec.org/j/G41.html

- https://www.sciencedirect.com/science/article/pii/S002243592500003X

- https://www.nber.org/papers/w30508

- https://www.sciencedirect.com/science/article/pii/S002243592500003X

- https://www.sciencedirect.com/science/article/pii/S0022435924000654

- https://ijsps.ism.gov.my/IJSPS/article/view/332

- https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4198320

- https://www.studocu.vn/vn/document/truong-dai-hoc-tai-chinh-marketing/nghien-cuu-khoa-hoc/19336-1318-64894-2-10-20220901/116196416

References

Ashby, N. J. S., et al. (2025). The influence of the buy-now-pay-later payment mode on consumer spending decisions. Journal of Consumer Research.

Di Maggio, M., Williams, J., & Katz, J. (2022). Buy now, pay later: Impact on consumer spending. Journal of Financial Economics.

Jose, R., et al. (2025). Buy now, spend more, pay later: Behavioural mechanisms of buy now pay later products. Research technical paper.

Kumar, V., Salo, J., & Bezawada, R. (2024). The effects of buy now, pay later (BNPL) on customers’ online purchase behavior. Journal of Marketing Research.

Nusir, M., et al. (2026). The psychology of BNPL: A systematic review of impulsive buying and post-purchase regret (2018–2025). Journal of Behavioral Finance.

Rafidarma, D., & Aprilianty, F. (2022). The impact of buy now pay later feature towards online buying decision in e-commerce Indonesia. International Journal of Business and Management Studies.

Sarifuddin, S. H. (2024). Buy now, pay later or pain later? A qualitative study on the adoption of BNPL and financial risks among Generation Z consumers in Klang Valley. Asian Journal of Consumer Studies.

Simolinna, K. (2025). The influence of buy now, pay later services on consumer spending behavior (Bachelor’s thesis). University publication.

Agarwal, S., Chomsisengphet, S., Liu, C., & Souleles, N. S. (2021). Benefits of relationship banking: Evidence from consumer credit markets. Journal of Monetary Economics, 117, 323–339.

Baker, S. R., Farrokhnia, R. A., Meyer, S., Pagel, M., & Yannelis, C. (2023). Income, liquidity, and the consumption response to the 2020 economic stimulus payments. Review of Financial Studies, 36(6), 2381–2418.

Falk, A., & Szech, N. (2013). Morals and markets. Science, 340(6133), 707–711.

Gathergood, J., & Weber, J. (2017). Financial literacy, present bias and alternative mortgage products. Journal of Banking & Finance, 78, 58–83.

Prelec, D., & Loewenstein, G. (1998). The red and the black: Mental accounting of savings and debt. Marketing Science, 17(1), 4–28.

Raghubir, P., & Srivastava, J. (2008). Monopoly money: The effect of payment coupling and form on spending behavior. Journal of Experimental Psychology: Applied, 14(3), 213–225.

Soman, D. (2001). Effects of payment mechanism on spending behavior: The role of rehearsal and immediacy of payments. Journal of Consumer Research, 27(4), 460–474.

Thaler, R. H. (1999). Mental accounting matters. Journal of Behavioral Decision Making, 12(3), 183–206.

Zhang, Y., & Sussman, A. B. (2018). The role of mental accounting in household spending and saving decisions. Journal of Consumer Psychology, 28(3), 357–372.

Zinman, J. (2015). Household debt: Facts, puzzles, theories, and policies. Annual Review of Economics, 7, 251–276.