Abstract: The rapid digitalisation of financial services has transformed the global banking landscape, resulting in emergence of neo-banks as technology-driven alternatives to traditional banking institutions. This study examines the impact of global neo-banking expansion and domestic digital ecosystem factors on the growth of neo-banks in India, with particular emphasis on user adoption and profitability. The research addresses the existing gap in empirical literature by analysing whether macro-level indicators such as global neo-bank transaction value, internet penetration, UPI transaction value, and fintech funding significantly influence neo-bank performance in India. The primary aim is to give a data-driven evaluation of the structural drivers shaping the development of neo-banking within an evolving regulatory and technological environment. The study takes into consideration a quantitative research design using secondary time-series data covering the period from 2018 to 2025. Data has been taken from reliable institutional and industry sources including regulatory bodies and financial databases to ensure objectivity and consistency. Statistical tools like descriptive statistics, correlation analysis, regression models, multicollinearity testing, and trend analysis are employed to analyse relationships between independent variables and neo-bank growth indicators. The findings show that global neo-banking growth is a decisive factor influencing both user adoption and profitability of neo-banks in India, highlighting strong spillover effects from international fintech expansion. Internet penetration and UPI transaction activity function as key enablers of digital financial services, strengthening adoption levels. However, the results interpret that profitability lags behind user growth, suggesting that Indian neo-banks currently prioritize scale over immediate financial sustainability. Additionally, fintech funding demonstrates a weak direct relationship with performance outcomes, implying that capital inflows alone do not guarantee long-term success without efficient monetisation strategies.

Overall, the study concludes that neo-bank development in India is shaped by the combined influence of global expansion and domestic digital readiness, highlighting the need for balanced strategies that focus on both customer acquisition and sustainable revenue generation.

Key Words: Neo-banking, Digital Ecosystem, Fintech Growth, User Adoption, Profitability

1. Introduction:

The Indian banking and financial services sector is undergoing a significant transformation driven by rapid digitalisation, technological innovation, and changing consumer preferences. Traditional banking systems, which rely heavily on physical branches and manual processes, are increasingly being complemented and challenged by digital financial institutions known as neo-banks. These banks operate primarily through mobile and web-based platforms, offering streamlined, low-cost, and customer-centric financial services without maintaining extensive physical infrastructure. Their technology-driven business models enable faster service delivery, personalised financial solutions, and reduced operational costs, making them very attractive to digitally savvy consumers.

Globally, neo-banks such as WeBank, Monzo, and Nubank have demonstrated strong growth potential by enhancing financial inclusion and achieving operational efficiency. In contrast, the Indian neo-banking ecosystem is still evolving and operates within a distinct regulatory framework. Indian neo-banks do not possess independent banking licenses from the Reserve Bank of India and instead function through partnerships with licensed banks and Non-Banking Financial Companies (NBFCs) to deliver core banking services. While this partnership model enables operational continuity, it also raises concerns regarding autonomy, scalability, and long-term sustainability.

India’s favourable digital environment, supported by rising internet penetration, common smartphone adoption, expansion of the Unified Payments Interface (UPI), and increasing fintech investments has created strong conditions for neo-bank adoption. Despite notable growth in user adoption and transaction volumes, there is limited empirical evidence on whether these digital and global factors translate into sustainable growth and profitability for Indian neo-banks. Much of the existing discussion is descriptive and does not adequately evaluate the economic outcomes of neo-banking expansion.

Therefore, this study examines the impact of global neo-banking expansion and domestic digital ecosystem variables on the growth of neo-banks in India empirically. Using secondary data over an eight-year period, the research seeks to remove the gap between descriptive adoption narratives and data-driven evaluation of neo-bank performance, providing meaningful insights into whether neo-banks can emerge as sustainable and transformative players within the Indian banking sector.

1.1 Need of the Study

The emergence of digital financial services has led to a paradigm shift in the global banking sector, positioning neo-banks as a popular digital alternative to traditional financial institutions. Although neo-banks have achieved notable success in several countries, their development in India presents a unique scenario shaped by regulatory constraints, evolving consumer behaviour, and the structure of the domestic digital payment infrastructure. While neo-banks in India continue to gain popularity and expand their customer base, there is a lack of empirical research examining the factors that impact their growth and financial performance.

Most existing literature on neo-banking in India primarily focuses on customer awareness, adoption patterns, and qualitative assessments of technological innovation. However, there is limited comprehensive research that applies data-driven methods to analyse how global neo-banking expansion and domestic digital ecosystem variables—such as internet penetration, UPI transaction growth, and fintech funding—affect the growth and profitability of neo-banks. This gap restricts the ability of policymakers, regulators, and industry stakeholders to accurately evaluate the long-term viability and sustainability of neo-banking within the Indian financial system.

Furthermore, Indian neo-banks operate through partnership models due to the absence of standalone banking licenses, raising important concerns related to scalability, operational independence, and the capacity to achieve sustainable profitability. Understanding macro-level digital and financial trends is therefore essential for assessing the growth outcomes of neo-banks and their potential role in the future of banking in India.

1.2 Aim of the Study

The primary aim of this study is to analyse the impact of global neo-bank growth and the expansion of India’s digital financial ecosystem on the development of neo-banks in India, with particular focus on user adoption and average profitability. The study investigates whether rapid global neo-banking expansion, together with domestic digital enablers such as internet penetration, digital payment infrastructure, and fintech funding, has significantly contributed to the performance of neo-banks in the country.

By adopting a data-driven empirical approach, the research moves beyond descriptive assessments and provides quantitative insights into the factors influencing neo-bank growth in the Indian context while incorporating global developments.

1.3 Scope of the Study

This study focuses on the growth of neo-banks in India during the period 2018–2025, a phase marked by rapid digitalisation and fintech expansion. It uses secondary data from trusted sources such as RBI, NPCI, and Statista to analyse macro-level factors including global neo-bank transaction value, internet penetration, UPI transaction value, fintech funding, user growth, and profitability.

The research adopts an industry-level perspective and does not examine individual firms, consumer behaviour, or international comparisons. Therefore, the findings provide broad insights into the key drivers influencing neo-bank development in India rather than firm-specific conclusions.

1.4 Problem Statement

Neo-banks have emerged as major disruptors in the global banking sector; however, their growth trajectory in India remains uncertain due to regulatory dependence on licensed banks and NBFC partnerships. Despite improvements in digital infrastructure such as rising internet usage, UPI transactions, and fintech investments, there is limited to no empirical evidence regarding how these factors influence neo-bank user adoption and profitability.

Existing studies largely focus on customer perception and industry trends, creating a research gap in understanding the quantitative relationship between digital ecosystem variables and neo-bank growth. Addressing this gap is essential to evaluate the long-term sustainability of neo-banks in India.

1.5 Objectives of the Study

- To analyse the influence of digital ecosystem factors such as internet penetration, UPI transaction value, and fintech funding on neo-bank growth in India.

- To evaluate the impact of global neo-bank expansion on user adoption and financial performance of Indian neo-banks.

- To examine the overall expansion of neo-banks within India’s financial ecosystem.

II. Review of Literature

Shabu and Vasanthagopal (2021) focused on exploring the opportunities and challenges related to neobanks in India through observing customer perception based on Tweets under hashtags like ‘#neobank’ which was viewed and filtered to have 1,730 Tweets, out of which 472 out of 492 responses were observed to have a “very positive” sentiment towards ‘neobank’ related to convenience, innovation, etc., as offered in India. Challenges associated with neobanks were inferred as limited financial options, lack of personal interactions in neobanks, issues concerning customer trust, and security of neobanks, keeping in view opportunities such as instant fund transfer, international remittances, personal financial information, and innovative savings options offered by neobanks in India. The authors concluded that although neobanks in India have strong acceptability from both existing and prospective customers, for neobanks in India to achieve sustainable success, it is important to address issues such as enhanced security systems and financial literacy of Indian citizens.

Adityadev & Jagadeesh (2023) researched customer perception regarding neo-banking services across India by conducting a survey among 180 people residing in Mangalore. The experts observed, although many people are aware of the advantages of neo-banking services, like their cost-effectiveness and relative safety, many are still unaware of its full capabilities. The results obtained during the course of this survey indicated that though 40% people were willing to shift to neo-banking services, they could not afford to get personal services from neo-banking service providers. The experts concluded that awareness campaigns regarding neo-banking services will play a crucial role towards accepting neo-banking services as substitutes to conventional banking services.

Arun et al. (2023) examined the activities of neo-banks in India and the UK, where India has 36+ players operating with partnership models owing to regulatory issues with the Reserve Bank of India, whereas banks such as Monzo and Revolut in the UK enjoy operating independently. Financial inclusion, along with opportunities in open banking, were also an important part of such studies, along with challenges such as low margins, cybersecurity issues, etc., along with investors facing issues with neo-banks. Acumen in case studies addressed strategic models such as sandboxes in order to operate in an eco-friendly manner, with regulation, along with strong cybersecurity measures, being important in order to sustain in such an arena in the long run.

Sardar and Anjaria (2023) described the impact of the emergence of neo-banks upon the banking industry of India with the help of the descriptive survey method using a sample size of 200 customers with chi-square test findings about the impact upon the banking industry of India with the emergence of the new dimension of the utility of bank accounts offered by neo-banks to customers about the features offered by the bank to its customers in relation to the ease of opening accounts with the bank, budgeting, payment utilisation of the large majority of the population with regard to the younger section of the population in relation to the utility of the banking facility offered by the bank to its customers in relation to the features offered by the bank to the new customers with the emergence of the new dimension.

Sowjanya (2023) researched the concept of the emergence and growth of neo-banks in India, which are fully digital financial services providers offering speed, savings, and round-the-clock services to the population, differentiating themselves from brick-and-mortar banks operating in the country. Though the financial services industry come across challenges like RBI regulations, limited services provided, and costly customer acquisitions, the researcher has found, given the projected worth of the neo-banks’ market surpassing the USD 600 Billion mark by the year 2028, even after a pandemic like COVID-19 attributing to the trend, these financial services are the future of the country’s banking industry.

Sharanya & Shailaja (2023) undertook a cross-country comparison of neo-banking in India and the US, identifying differences in their adoption, regulation, and consumer trust. Based on their descriptive study, it was established that in spite of these challenges confronting neo-banking in India, which include ambiguity in regulations, dependence on banking partners, as well as low consumer financial literacy, there is huge potential, given the fact that this is a rapidly adopting market, with UPI in place. They concluded their paper by showing that, in spite of these prospects, the future of neo-banking in India is subject to improvements in regulations, security measures, as well as consumer understanding.

Maryna et. al. (2023) explored the transformation of the banking sector in Switzerland in relation to neobanks. Based on their analysis, they demonstrated examples of how neobanks, being digital banks, alter the banking sector in Switzerland by providing low-cost, innovative, and consumer-friendly banking services. Based on a qualitative analysis, the researchers analysed that although there are hurdles in the development of neobanks in Switzerland, these banks are a promising driver of the industry.

Ziouache & Bouteraa (2023) offered a theoritical study on the development conception, disadvantages, and global practices concerning neo-banks. In the study, the authors presented differences in the meanings of neo-banks, traditional banks, and digital banks. Neobanks have various advantages such as lower costs, real-time presence, and the ability to advance financial inclusion. Additionally, the study presented the disadvantages associated with neo-banks. Using the Technology Acceptance Model (TAM), with the incorporation of trust and security, the study found the two variables to play an integral role in the adoption of neo-banking as a new form of banking. The study on neo-banks indicated that the banking sector is in its infancy in the global community. Therefore, it is necessary to build trust and security in the adoption of neo-identity.

Rathod and Purey (2023) carried out a study where they conducted a literature review concerning customer awareness and preference toward neobanking services. The study showed that customer awareness dominantly revolves around young populations with a high degree of urbanization, while customer adoption revolved around aspects such as convenience, cost-effectiveness, and ease of use together with the integration with mobile devices.

Au (2024) studies the sustainability and risks of neobanks with the help of a case study on Nubank and StoneCo operating in Brazil. The case study adopted different valuation models with information relating to financial reports and earnings. The case study found Nubank was overvalued and StoneCo undervalued. This signified the risks and volatility associated with the business models adopted by neobanks. The risks associated with neobanks include firm-specific risks regarding cumulative operating costs, elevated borrowing costs, and unsteady margins. The case study also revealed risks regarding political risks, exchange rate risks, and equity risks. The research decided that even though neobanks have managed to enhance access and customer trust, their equity-based financing and underlying risks for emerging markets are associated with poor prospects for their long-term sustainability.

Sharma (2024) conducted a study comparing neo-banks and traditional banks. Based on the study, neo-banks are characterized by low costs, technology-enabled banking, and customer-centricity. Moreover, neo-banks have managed to attract young consumers following the low costs and personalized experiences offered. In the study, traditional banks are characterized by product-centricity, dependents of physical branches, and high costs. In the study, transaction value in the neo-banking industry in India is expected to reach US$122.3 billion by the year 2027. In essence, it shows how neo-banks complement traditional banks as competitors.

Chandran et. al. (2025) analysed in depth the fast increase of neobanks in India with both qualitative and quantitative methods of research for conducting market trend studies, consumer adoption studies, and overcoming issues such as government regulations. With such studies utilizing secondary data analysis methods, it has explained that smartphone usage rate, Internet access, along with government-backed initiatives such as UPI and Jan Dhan Yojana, have facilitated faster adoption of neobanks in India, with increasing consumer adoption rate rising to 26% of India’s population in 2023. Though neobanks have facilitated faster financial inclusions in India, issues such as trust factor, secured systems, etc., still prevail along with government regulation issues, with such studies pointing towards an increasing trend of neobanks in India with rising transactional volumes with an estimated CAGR of 27.1% until 2026.

Kedla et al. (2025) studies about the phenomenon of neo-banks rising in India with digital-only services including instant account opening, enabling transactions in different currencies, payroll management, loans, and investments. Opportunities include the population in rural India mostly who do not have a bank account, while challenges include a lack of regulations, cybersecurity threats, poor financial literacy, and the use of cash. The report states that despite all the challenges, cooperation with NBFCs and conventional banks makes neo-banks an integral component of India’s financial landscape.

Hussain and Zaman (2025) investigated the risks which result in the failure of neo-banking in Pakistan from an economical, political, regulatory, and compliance perspective. From a survey done on 225 participants and regression results, a high positive correlation was noted, r=0.682, p < 0.01, where 46.5% of the causes were accounted for through risks leading to failures; thus, this study demonstrates how sustainability is marred by stability issues, regulatory requirements, and cybersecurity risks, among other sustainability threats to neo-banking.

Kushwaha & Malpani (2025) examined the effect of Fintech on financial inclusion in India by using panel data from 28 states, ranging from 2015 to 2023. The authors developed a multidimensional inclusion index using fixed-effects regression and noticed significant improvement in access and usage of finances, especially in less-developed and rural parts of the country, due to digital payment growth. Additionally, it was observed that there is a reduced gender gap in inclusion and increased access to credit for the unbanked. Ending, the major conclusion derived is that Fintech improves inclusion primarily through expansion in the dimension of access and use rather than quality of service.

Yadav and Sandhu (2025) analyzed the opportunities and challenges of neo banks in the context of the Indian market, using a descriptive research methodology, depending upon secondary data and a comparative analysis of 12 most prominent neo banks. Based upon their analysis, it is clear that opportunities of neo banks include their capability to attract more customers by providing low-cost, tech-savvy services, 24\7 availability, budgeting, automation, and making international transactions. However, their major problems include areas such as no banking license, ambiguity of rules and regulations, cybersecurity, and trust building, especially when it comes to handling low-income, low-digitally literate individuals. Their study concluded that neo banks would exist side by side with traditional banks, yet there needs to be an effective handling of areas such as privacy, security, and rules.

Badre (2024) reviewed literature related to remittances, digital financial inclusion, and neo-banks, specifically in relation to the North African-European Union migration corridor. The literature provided an overview of how neo-bank players, such as Wise, N26, Revolut, shape international money transfers by reducing transactional costs, enhancing convenience, and offering customer-focused service delivery models, even though remnants of hindrances such as trust issues, low digital literacy, and regulatory requirements remain, restraining migrants from taking advantage of neo-bank service delivery models. The literature concluded that, despite the above, a clear need existed to examine the link that neo-bank service delivery models create, relating to financial inclusion value propositions aimed at reducing transactional costs of international remittances, specifically relating to vulnerable migrant groups.

Citterio et. al. (2024) investigated the early growth and evolution of neobanks, as they are known in Europe, by matching 65 fully licensed digital-only banks with their 313 traditional counterparts. The results revealed that neobanks perform less than their peers by offering lower returns due to their higher levels of impaired charges and operating expenses, even though their risks are comparable. However, this study revealed good examples of economies of scale and scope for larger neobanks that will help mitigate their initial inefficiencies.

Bhatnagar and Rajesh (2024) studied the adoption of neo-banking in India by incorporating perceived risks in the UTAUT3 model. Using a survey of 680 users in the Delhi NCR area of India that incorporated PLS-SEM analysis, it was established that performance expectancy, effort expectancy, and facilitating conditions were adoption drivers, although privacy and performance risks were deterring factors in adoption. Notably, the model demonstrated an explanatory rate of over 70% variance in adoption or usage, pointing to the attractiveness of convenience as well as the demotivating effects of issues of trust in suitability.

Neog and Ahmed (2025) investigated the concept of neo banking in India together with social inequality from a qualitative theory-driven viewpoint. The study adopted Social Exclusion Theory and Bourdieu’s Theory of Capital as guidelines in understanding data from secondary sources of RBI, NPCI, and other literature to determine “whether neo banking is an opportunity beyond financial barriers, particularly for social excluded groups in India, or just fuelling social inequality due to digital illiteracy, lack of infra, and lack of trust in the concept.” By supporting case study research conducted on neo banking platforms such as Jupiter, Fi Money, and Niyo X, the authors conclude “with the emergence of neo banking in India, it is very important to address social inequality factors in order to take its true benefits to society.”

2.1 Research Gap

Existing literature on neo-banking primarily focuses on customer perception, adoption behaviour, service quality, and technological advantages, particularly within the Indian context. However, these studies depend heavily on descriptive and qualitative approaches, providing limited empirical evidence on how macro-level factors influence measurable growth outcomes.

International research has examined valuation, risk, and sustainability of neo-banks, but such findings cannot be directly applied to India due to differences in regulatory structures and the partnership-based operating model followed by Indian neo-banks. Additionally, although factors such as internet penetration, UPI adoption, and fintech initiatives are widely acknowledged as important, they are rarely tested using quantitative frameworks.

Moreover, prior studies often analyse user adoption and profitability separately, creating a gap in understanding whether adoption-driven expansion translates into financial sustainability. There is also limited research investigating the influence of global neo-banking expansion on domestic neo-bank growth in emerging economies like India.

Therefore, this study addresses the need for an empirical, macro-level analysis that quantitatively evaluates the impact of global neo-banking growth and domestic digital ecosystem variables on user growth and profitability of neo-banks in India.

III. Research Methodology

This study adopts a quantitative research approach to examine the impact of global neo-banking expansion and domestic digital ecosystem factors on the growth of neo-banks in India. The research is based entirely on secondary time-series data covering the period from 2018 to 2025. A macro-level analytical framework is used to identify relationships between selected independent variables and growth indicators such as user adoption and profitability. Statistical techniques are applied to ensure objective evaluation and support empirical findings.

3.1 Data Collection and Sources

The study relies exclusively on secondary data collected from credible institutional and industry sources. Key data providers include the Reserve Bank of India (RBI) for digital banking trends, the National Payments Corporation of India (NPCI) for UPI transaction data, and Statista along with industry reports for global neo-bank transactions, fintech funding, and user statistics. The use of verified datasets enhances reliability, comparability, and overall validity of the research.

3.2 Sampling Type and Size

The research follows a non-probability judgmental sampling technique, as the study is based on secondary data rather than individual respondents. Annual observations from 2018–2025 are selected intentionally to represent the post-digitalisation phase of India’s financial sector. Each year constitutes one observation, resulting in a sample size of eight time-series data points for both independent and dependent variables.

3.3 Hypothesis

H1: Global neo-bank transaction value significantly impacts neo-bank user growth in India.

H2: Global neo-bank transaction value significantly impacts the profitability of neo-banks in India.

H3: Internet penetration in India significantly influences neo-bank user growth.

H4: Internet penetration significantly affects the profitability of neo-banks.

H5: UPI transaction value significantly impacts neo-bank user growth in India.

H6: UPI transaction value significantly affects neo-bank profitability.

H7: Fintech funding significantly influences neo-bank user growth in India.

H8: Fintech funding significantly affects the profitability of neo-banks.

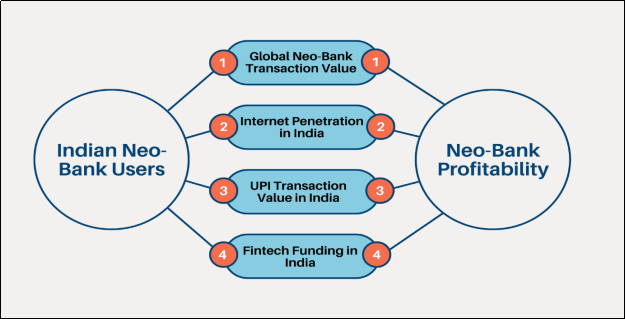

3.4 Variables

The study categorizes variables into independent and dependent groups to examine their relationship with neo-bank growth.

Figure 6: Variable Model

Independent Variables:

- Global neo-bank transaction value: This variable is used as an indicator of worldwide neo-banking expansion and reflects the level of technological maturity, adoption, and trust in digital-only banking models. Since Indian neo-banks often adapt global fintech innovations, this variable captures possible international spillover effects.

- Internet penetration in India: This variable represents the extent of digital access among the Indian population. As neo-banks only operate through digital platforms, such as an app or a website which requires internet, and hence, the availability of the internet becomes a fundamental prerequisite for adoption and usage.

- UPI transaction value: This variable shows the intensity of digital payment activity in the economy. UPI is considered the backbone of neo-bank transactions and customer engagement, which makes it a key driver of neo-bank usage growth.

- Fintech funding: This variable reflects the level of financial resources that are available to fintech and, hence, their subset, neo-banking firms, for technology development, marketing and expansion. This variable helps assess whether the investment made is translating into operational growth and profitability.

Dependent Variables:

- Neo-bank user growth in India: Neo-bank user growth shows the increase in the number of customers for neo-banking platforms. This concept is commonly referenced in fintech literature as an important indicator of adoption and market acceptance.

- Average profitability of leading neo-banks: Average profitability shows how well neo-banking platforms perform financially and how sustainable they are. Previous research on neo-banks and fintech companies points out that profitability usually falls behind user growth because of high costs for acquiring customers and technology.

All variables are operationally defined and measured using industry-level data to maintain consistency and support statistical analysis.

3.5 Method of Data Collection and Sources

All the data used in its current form is secondary data since the main aim of the research is to examine macro-level trends and relationships that affect the development of the neo-banks in India. It is believed that secondary data are suitable to this research since it will be possible to explore the patterns observed in the industry over the long term with the help of standardised and reliable and publicly accessible datasets. The information employed in the study is culled out of the institutional, regulatory, and industry sources of information which are authoritative and they are reliable and credible. The secondary data sources offer validated information that is common in academic studies, policy formulation, and reporting in industries, which increases the credibility and validity of the study.

The major data resources that will be used in the study are:

- Reserve Bank of India (RBI): Sources of information on the trends of digital banking, fintech trends, indicators of the payment system, and regulatory environment.

- National Payments Corporation of India (NPCI): This is applied to yearly data on UPI transactions value, which are the digital payments in India.

- Statista: Applied to international neo-bank transaction value, fintech funding information, neo-bank user approximations and financial measures of the industry.

- Industry and international financial reports: These are reports intended to supplement the information on the growth, investment trends and profitability patterns of the neo-banking when such information is publicly disclosed.

All the gathered data concerns the time interval of 2018-2025 and is arranged in a systematic format to allow conducting statistical analysis. All the data was tabulated in spreadsheets and cross-corroborated wherever feasible with various sources in order to ascertain uniformity and lessen chances of measurement error.

The study is not primary data collection research based on surveys, interviews and questionnaires. It is also not based on the company-level financial statements or insider company revelations. The study is objective in its approach because it does not rely on primary data, but this implies that its view on the neo-banking industry in India is rather macro-level.

The data collected for the study involves data of global neo bank transaction value, UPI transaction value in India, Internet penetration in India and Fintech Funding in India as independent variables and for the dependent variables, the data collected shows the Indian users and the average profitability of the leading neo-banks in India. The data has been taken from verified sites such as TRAI, NPCI and Statista.

3.6 Sampling type and Size

This proposed research follows the non-probability sampling methodology, which is the judgmental (purposive) sampling technique because the researchers do not use personal respondents, but instead secondary data. The sampling in the context of empirical research which is based on secondary data is not about the choice of individuals or firms but rather a choice of the variables, timeframes and data points that represent the phenomenon under study optimally.

The study sample will include time-series observations annually within the 2018-2025. It has been chosen intentionally as this timeframe represents the post-digitalisation stage of the Indian financial industry, during which the digital payment market rapidly increases, fintechs become widespread, and neo-banks come into prominence as important digital financial intermediaries.

Industry level neo-bank user growth in India and the average profitability of the top neo-banks are dependent variables that are measured with aggregated data. The independent variables, which include the global neo-bank transaction value, internet penetration in India, UPI transaction value, and fintech funding in India are also measured with annual industry level data. The study period is one observation (one year) which makes the sample size of the variables eight annual observations.

This study employs judgmental sampling due to the deliberate nature of the data points to be used in the study in terms of relevance, accuracy, and consistency since the points are chosen based on authoritative and credible sources. This is the sampling that is often used in macroeconomic, financial, and industry level studies where the aim of the study is to examine trends and relationships over time, not to generalise the results of a population that has been selected randomly.

3.7 Statistical Design

The research employs multiple statistical tools to analyse the data. Descriptive statistics are used to summarise data characteristics, while correlation analysis examines the strength and direction of relationships between variables. Multiple regression models help determine the impact of independent variables on user growth and profitability. Additionally, multicollinearity is tested using the Variance Inflation Factor (VIF) to ensure stability of regression coefficients, and trend analysis is applied to observe growth patterns over time.

3.8 Limitations of the Study

The study is subject to certain limitations. First, it relies solely on secondary data, restricting control over data accuracy and collection methods. Second, the analysis is based on eight years of annual data, which may limit deeper insights into short-term fluctuations. Third, the macro-level approach does not capture firm-specific strategies or operational differences among neo-banks.

Additionally, the absence of primary data means behavioural aspects such as customer trust and satisfaction are not directly examined. Limited public disclosure on profitability also requires reliance on industry-level estimates rather than firm-level financial data.

IV. Analysis and Interpretation

Descriptive Statistics

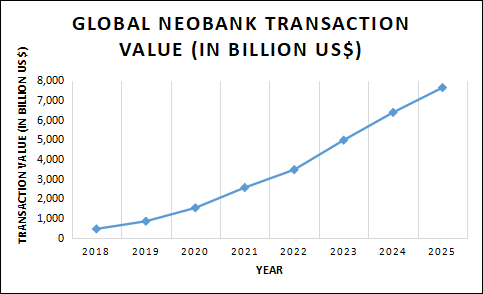

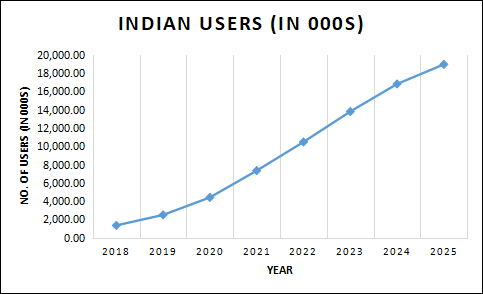

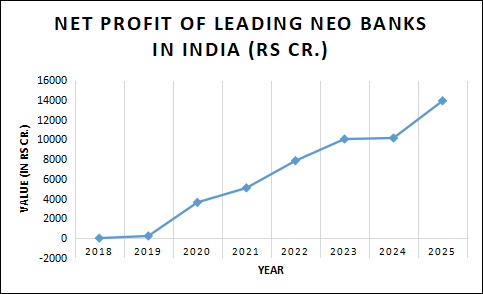

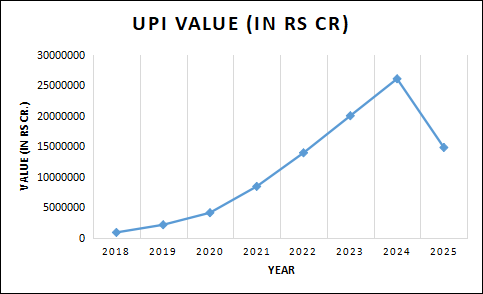

The descriptive analysis indicates strong growth in global neo-bank transactions, reflecting the rapid expansion of digital banking worldwide. Internet penetration in India increased steadily, supporting digital financial adoption, while UPI transaction value showed exponential growth, highlighting the shift toward cashless payments. Neo-bank user numbers rose consistently during the study period; however, profitability remained volatile, suggesting that the sector is still focused on scaling rather than achieving financial stability.

Table 1: Descriptive Statistics

Details of the survey questions are available in Table 1.

| Descriptive Statistics | Global Neo-Bank Transaction Value (in billion US$) | Internet Penetration (in mn) | UPI Value (in cr) | Fintech Funding (in billion US Dollars) | Indian Users (in 000s) | Net Profit of Leading Neo Banks in India (Rs. Cr.) |

|---|---|---|---|---|---|---|

| Mean | 3472.5 | 856.58375 | 11287438.15 | 3.60875 | 9449.9725 | 6359.939563 |

| Standard Error | 931.7988555 | 44.7228037 | 3177092.813 | 0.81271467 | 2344.798772 | 1766.133362 |

| Median | 3005 | 853.275 | 11169124.42 | 2.6 | 8900.485 | 6465.6875 |

| Standard Deviation | 2635.525158 | 126.495191 | 8986175.489 | 2.29870422 | 6632.09245 | 4995.379507 |

| Sample Variance | 6945992.857 | 16001.0334 | 8.07513E+13 | 5.28404107 | 43984650.27 | 24953816.42 |

| Kurtosis | -1.198422404 | -0.3048223 | -0.954608458 | 1.61638478 | -1.584939619 | -1.1635374 |

| Skewness | 0.472331432 | -0.5252076 | 0.434003197 | 1.4648283 | 0.216708029 | 0.042069643 |

| Range | 7180 | 381.08 | 25179983.93 | 6.7 | 17591.13 | 13922.62 |

| Minimum | 450 | 636.73 | 876970.72 | 1.6 | 1353.27 | -3 |

| Maximum | 7630 | 1017.81 | 26056954.65 | 8.3 | 18944.4 | 13919.62 |

| Sum | 27780 | 6852.67 | 90299505.16 | 28.87 | 75599.78 | 50879.5165 |

| Count | 8 | 8 | 8 | 8 | 8 | 8 |

Correlation Analysis

The results show a strong positive relationship between global neo-bank expansion and user growth in India, implying significant international spillover effects. Internet penetration and UPI usage also demonstrate positive associations with adoption, confirming the importance of digital infrastructure. In contrast, fintech funding exhibits a weak relationship with both adoption and profitability, indicating that investment alone does not guarantee performance improvements.

Table 2: Correlation Analysis

| Variables | Global NeoBank Transaction Value (in billion US$) | Internet Penetration (in mn) | UPI Value (in cr) | Fintech Funding (in billion US Dollars) | Indian Users (in 000s) | Net Profit of Leading Neo Banks in India (Rs. Cr.) |

|---|---|---|---|---|---|---|

| Global NeoBank Transaction Value (in billion US$) | 1 | |||||

| Internet Penetration (in mn) | 0.940512 | 1 | ||||

| UPI Value (in cr) | 0.859839 | 0.852963913 | 1 | |||

| Fintech Funding (in billion US Dollars) | -0.20447 | -0.07452947 | -0.13268 | 1 | ||

| Indian Users (in 000s) | 0.995442 | 0.953800512 | 0.893255 | -0.1598 | 1 | |

| Net Profit of Leading Neo Banks in India (Rs. Cr.) | 0.974513 | 0.964048559 | 0.841295 | -0.11077 | 0.98276 | 1 |

Regression Analysis

Regression findings identify global neo-bank transaction value as a key predictor of both user growth and profitability. Internet penetration significantly supports deeper usage and revenue generation, whereas UPI primarily drives adoption with limited influence on profits due to its low-margin nature. Fintech funding does not show a statistically significant impact, suggesting its role is more supportive than directly performance-driven.

Table 3: Regression Statistics: Neo-Bank Users In India

| Regression Statistics | |

|---|---|

| Multiple R | 0.999115767 |

| R Square | 0.998232316 |

| Adjusted R Square | 0.995875405 |

| Standard Error | 425.9329461 |

| Observations | 8 |

| ANOVA | |||||

|---|---|---|---|---|---|

| Source | df | SS | MS | F | Significance F |

| Regression | 4 | 307348295.3 | 76837074 | 423.5341 | 0.000185603 |

| Residual | 3 | 544256.6238 | 181418.9 | ||

| Total | 7 | 307892551.9 | |||

| Variables | Coefficients | Standard Error | t Stat | P-value | Lower 95% | Upper 95% | Lower 95.0% | Upper 95.0% |

|---|---|---|---|---|---|---|---|---|

| Intercept | -2382.3518 | 2795.7423 | -0.8521 | 0.4567 | -11279.6517 | 6514.948 | -11279.7 | 6514.948 |

| Global NeoBank Transaction Value (in billion US$) | 2.0776 | 0.2052 | 10.1229 | 0.0020 | 1.4245 | 2.7308 | 1.4245 | 2.7308 |

| Internet Penetration (in mn) | 3.7891 | 4.1271 | 0.9181 | 0.04262 | -9.3452 | 16.9235 | -9.3452 | 16.9235 |

| UPI Value (in cr) | 9.2849 | 3.629 | 2.5584 | 0.0833 | -2.2644E-05 | 0.0002 | -2.3E-05 | 0.0002 |

| Fintech Funding (in billion US Dollars) | 89.7221 | 76.5035 | 1.1727 | 0.3255 | -153.7461 | 333.1906 | -153.746 | 333.1906 |

Table 4: Regression Statistics: Neo-bank profitability

| Regression Statistics | |

|---|---|

| Multiple R | 0.985917 |

| R Square | 0.972031 |

| Adjusted R Square | 0.93474 |

| Standard Error | 1276.123 |

| Observations | 8 |

| ANOVA | |||||

|---|---|---|---|---|---|

| Source | df | SS | MS | F | Significance F |

| Regression | 4 | 1.7E+08 | 42447811 | 26.06575 | 0.011497335 |

| Residual | 3 | 4885470 | 1628490 | ||

| Total | 7 | 1.75E+08 | |||

| Variables | Coefficients | Standard Error | t Stat | P-value | Lower 95% | Upper 95% | Lower 95.0% | Upper 95.0% |

|---|---|---|---|---|---|---|---|---|

| Intercept | -11127.4 | 8376.227 | -1.32845 | 0.276045 | -37784.27894 | 15529.51 | -37784.3 | 15529.51 |

| Global NeoBank Transaction Value | 1.27576 | 0.61493 | 2.074643 | 0.012966 | -0.681221359 | 3.232742 | -0.68122 | 3.232742 |

| Internet Penetration | 15.25103 | 12.36517 | 1.233386 | 0.030526 | -24.10044923 | 54.6025 | -24.1004 | 54.6025 |

| UPI Value (in cr) | -3.4E-05 | 0.000109 | -0.30952 | 0.077718 | -0.000379681 | 0.000312 | -0.00038 | 0.000312 |

| Fintech Funding (in billion US Dollars) | 103.4512 | 229.2096 | 0.451339 | 0.682375 | -625.996026 | 832.8984 | -625.996 | 832.8984 |

Multicollinearity Analysis

Variance Inflation Factor (VIF) results reveal some interdependence among digital ecosystem variables, particularly those related to transaction activity and digital adoption. However, the multicollinearity is not severe enough to affect the reliability of the regression models.

Trend Analysis

Trend patterns reveal a steady rise in global neo-banking activity and Indian neo-bank users, particularly after 2020, reflecting accelerated digital adoption. Although profitability shows gradual improvement, fluctuations indicate that financial sustainability is still evolving.

Figure 1: Trend Analysis of Global Neo-bank Transaction Value

Figure 2: Trend Analysis of Indian Neo-bank Users

Figure 3: Trend Analysis of Net Profit of Leading Neo Banks in India

Figure 4: Trend Analysis of UPI Transaction Value

Overall Interpretation

The analysis confirms that global expansion and domestic digital readiness are major drivers of neo-bank growth in India. While user adoption is strong, profitability continues to lag, emphasizing the need for strategies that balance rapid expansion with sustainable revenue generation.

V. Findings and Suggestions

The study reveals that global neo-banking expansion is a major driver of neo-bank growth in India, significantly influencing both user adoption and financial performance. Strong digital infrastructure, particularly rising internet penetration, has further supported the expansion of neo-banking services by improving accessibility and usage.

UPI transaction growth has played a crucial role in encouraging adoption by increasing consumer familiarity with digital payments; however, its contribution to profitability remains limited due to low transaction margins. The analysis also shows that fintech funding has no strong direct impact on growth or profitability, indicating that investment alone is insufficient without effective operational strategies.

Although neo-bank users have increased consistently, profitability remains unstable, suggesting that most neo-banks are currently prioritizing customer acquisition and scale over immediate financial sustainability. Overall, the findings indicate that neo-bank development in India is shaped by both global fintech trends and domestic digital readiness, but long-term success will depend on the ability to convert adoption into sustainable revenue.

5.1 Suggestions

Based on the findings of the study, it is recommended that regulators provide greater clarity and flexibility in neo-banking regulations to support scalability and long-term sustainability. Neo-banks should shift their strategic focus from rapid customer acquisition toward revenue-driven models by introducing value-added services and diversified income streams. Adopting global best practices in digital innovation and operational efficiency can further enhance competitiveness within the evolving financial landscape. While digital payment infrastructure such as UPI has supported adoption, neo-banks must strengthen customer engagement and monetisation strategies to improve profitability. Additionally, fintech funding should be utilized more effectively for technology development, risk management, and operational improvements rather than short-term expansion. Finally, continuous emphasis on cybersecurity, consumer trust, and financial literacy will be essential to ensure stable and sustainable growth of neo-banks in India.

VI. Conclusion

This study examined the impact of global neo-banking expansion and domestic digital ecosystem factors on the growth of neo-banks in India using secondary data from 2018 to 2025. The findings highlight that neo-banks have emerged as an important component of the evolving financial landscape, driven by rapid digitalisation, increased internet accessibility, and the widespread adoption of digital payment systems. Global neo-banking activity was identified as a significant determinant of both user adoption and financial performance, indicating the presence of strong international spillover effects on the Indian market.

The study also establishes that internet penetration and digital payment infrastructure act as key enablers of neo-bank growth by improving access and encouraging usage. However, while adoption levels have increased consistently, profitability has not progressed at the same pace. This suggests that many neo-banks are currently operating in a scale-focused phase, prioritizing customer acquisition over immediate financial returns. Furthermore, the limited direct impact of fintech funding implies that capital inflows alone cannot ensure long-term success without efficient monetisation and sustainable business models.

Overall, the growth of neo-banks in India is shaped by the combined influence of global fintech developments and domestic digital readiness. For neo-banks to achieve long-term sustainability, it is essential to balance expansion strategies with revenue generation and operational efficiency. The study contributes to a better understanding of the structural drivers of neo-bank growth and emphasizes the importance of adopting strategies that support both innovation and financial stability within India’s digital banking ecosystem.

References:

Ziouache, Alaeddine & Bouteraa, Mohamed. (2023). Descriptive Approach of Neo-Banking System: Conception, Challenges and Global Practices. International Journal of Business and Technology Management. 5. 194-204. 10.55057/ijbtm.2023.5.2.18.

Kedla, S., Tarun, & Asha, N. (2025). Fintech and the Future of Banking: The Rise of Neobanks and Digital-Only Financial Institutions. Scientia. Technology, Science and Society, 2(3), 63-67. DOI: 10.59324/stss.2025.2(3).06

Pooja Yadav and Akasha Sandhu (2025); NEO BANKING-EXPLORING OPPORTUNITIES AND CHALLENGES IN THE DIGITAL REVOLUTION Int. J. of Adv. Res. (Feb). 11-18] (ISSN 2320-5407). www.journalijar.com

V, A. V., & B, J. (2023). A STUDY ON CUSTOMERS PERCEPTION TOWARDS NEO BANKING SYSTEM. International Journal of Research -GRANTHAALAYAH, 11(4), 58–65. https://doi.org/10.29121/granthaalayah.v11.i4.2023.5116

Citterio, A., Marques, B.P. & Tanda, A. The Early Days of Neobanks in Europe: Identification, Performance, and Riskiness. J Financ Serv Res (2024). https://doi.org/10.1007/s10693-024-00433-x

Au, A. Neobanks in emerging markets: a risk assessment. Humanit Soc Sci Commun 11, 655 (2024). https://doi.org/10.1057/s41599-024-03138-7

Anjaria, Kavit. (2023). THE FUTURE OF BANKING: HOW NEO BANKS ARE CHANGING THE INDUSTRY. https://www.researchgate.net/publication/391635458

Arun, Thankom and Markose, Sheri M. and Murinde, Victor and Kostov, Philip and Khan, Ahmed and Arı, Nihan and Goel, Varnika and Sethi, Rashika, Impact of Neo-Banks (Digital Banks): India – UK Comparison (May 18, 2023). Available at SSRN: https://ssrn.com/abstract=4452179 or http://dx.doi.org/10.2139/ssrn.4452179

Shabu, Kayva and Ramankutty, Vasanthagopal, Neobanking in India: Opportunities and Challenges from Customer Perspective (February 17, 2022). Proceedings of the International Conference on Innovative Computing & Communication (ICICC) 2022, Available at SSRN: https://ssrn.com/abstract=4037656 or http://dx.doi.org/10.2139/ssrn.4037656

Neog, D., & Ahmed, M. (2025). Neo-banking and society: Financial innovation and social inequality in India. International Journal for Multidisciplinary Research (IJFMR), 7(2), 1–7. https://www.ijfmr.com/

T.SOWJANYA , Neo Banking – A New Era of Financial Services, International Research Journal of Humanities and Interdisciplinary Studies (www.irjhis.com), ISSN : 2582-8568, Volume: 4, Issue: 2, Year: February 2023, Page No : 137-140, Available at : http://irjhis.com/paper/IRJHIS2302015.pdf

D.S, S., & M.L, S. (2024). A STUDY ON CROSS-COUNTRY ANALYSIS OF NEO BANKING: INDIA AND THE US. EPRA International Journal of Environmental Economics, Commerce and Educational Management. https://doi.org/10.36713/epra18397.

Sharma, S. “Digital Disruption in Banking: A Comparative Analysis of Neo Banks and Traditional Institutions”. International Journal of Management and Development Studies, vol. 13, no. 3, Mar. 2024, pp. 01-12, doi:10.53983/ijmds.v13n3.001.

Abdeslam Badre, “Impacts of neo-banks on North African migrants’ remittances and financial inclusion”, Scientific African, Volume 26, 2024, e02384, ISSN 2468-2276, https://doi.org/10.1016/j.sciaf.2024.e02384 (https://www.sciencedirect.com/science/article/pii/S2468227624003260)

Sharanya, D. S., & Shailaja, M. L. (2024, September 29). A study on cross-country analysis of neo-banking: India and the US. EPRA International Journal of Environmental Economics, Commerce and Educational Management, 11(9). https://doi.org/10.36713/epra18397

Kushwaha, D., & Malpani, D. (2025). The impact of fintech on financial inclusion in India: An empirical analysis of digital payment adoption and banking access. International Journal of Environmental Sciences, 11(12s), 218. https://doi.org/10.36713/epra18397

Hussain, U., & Zaman, S. U. (2025). Neo banks: Assessing risk factors contributing to their failures. Indus Journal of Social Sciences, 3(2), 200–216. https://induspublishers.com/IJSS/about

Chandran, P., Vinay, D., & Kumar, L. K. (2025). A study on neobanks in India. International Journal of Enhanced Research in Management & Computer Applications, 14(1), 37–43.

Puneett Bhatnagr, Anupama Rajesh; Neobanking adoption – An integrated UTAUT-3, perceived risk and recommendation model. South Asian Journal of Marketing 12 November 2024; 5 (2): 93–112. https://doi.org/10.1108/SAJM-06-2022-0040

Surpalsinh Rathod, Neelam Purey (2024) Awareness And Preference Of Neobanking- A Systematic Literature Review. Library Progress International, 44(3), 27789-27797

Khmara, M., & Kapliar, K. (2024). Transformation of banking activities in Switzerland: The influence of neo-banks and prospects for the development of the financial sector. Actual Problems of International Relations, (158), 97–103. https://doi.org/10.17721/apmv.2024.158.1.97-103

Digital India. (2026, January 26). Indian fintech sector to reach $420 billion by 2029: Digital payments body. https://www.digitalindia.gov.in/news_post/indian-fintech-sector-to-reach-420-billion-by-2029-digital-payments-body/

CFTE. (2021, November 24). Fintech companies in India | Full list 2023. https://blog.cfte.education/fintech-unicorns-in-india-full-list/

Statista. (n.d.). India: Estimated fintech market size by segment. https://www.statista.com/statistics/1372806/india-estimated-fintech-market-size-by-segment/

ICICI Direct. (2024, August 19). India’s fintech industry. https://www.icicidirect.com/research/equity/finace/indias-fintech-industry

Statista. (n.d.). Payments worldwide outlook (in USD). https://www.statista.com/outlook/fmo/payments/worldwide?currency=USD

National Payments Corporation of India. (n.d.). BHIM product statistics. https://www.npci.org.in/product/bhim/product-statistics

Reserve Bank of India. (n.d.). Home page. https://www.rbi.org.in/

Statista. (n.d.). Fintech in India. https://www.statista.com/study/68286/fintech-in-india/

The Digital Fifth. (n.d.). Retail Neo Banks in India: Trends, Challenges & Innovation. The Digital Fifth. https://thedigitalfifth.com/retail-neo-banks-innovation-trends/

Impact of the LIFO Inventory Valuation on the 2005 Consolidated Results of the LOTOS Group – Investor Relations – LOTOS.pl. https://inwestor.lotos.pl/en/1186/p,972,i,233/reports__key_data/current_reports/impact_of_the_lifo_inventory_valuation_on_the_2005_consolidated_results_of_the_lotos_group

Yao, L., Li, M., Su, K., Wang, M., Duan, W., Wen, Y., & Wen, Y. (2024). Empowering Forestry Management and Farmers’ Income Growth Through the Digital Economy—Empirical Evidence from Guizhou Province, China. Forests, 15(11), 1998.

How Would Cashless India Work | Robots.net. https://robots.net/fintech/how-would-cashless-india-work/

Ohata, N., Uto, K., Shoda, F., Kuramoto, K., Shirao, M., Okada, N., Yanagisawa, T., & Aruga, H. (2016). Extended-Temperature Operation (−40 °C to +95 °C) of an EML TOSA Employing an Athermal Optical System. IEEE Photonics Technology Letters. https://doi.org/10.1109/lpt.2015.2506266

India’s Fintech Industry – ICICIdirect. https://www.icicidirect.com/research/equity/finace/indias-fintech-industry

UPI Volume Declines November – StartupTalky- Business News, Insights and Stories. https://startuptalky.com/tag/upi-volume-declines-november/

Sachar Committee – Wikipedia. https://en.wikipedia.org/wiki/Sachar_Committee

Syukeri, M., & Rafli, M. R. (2024). Planting new seed in a burned-out land: Making money from carbon credits in Kalimantan. https://core.ac.uk/download/622242142.pdf

UPI clocks 6.57 Bn transactions in August. https://entrackr.com/2022/09/upi-clocks-6-57-bn-transactions-in-august/

Jacob, J., & Abubakar, S. (2015). Power Sector Viability and Development in Nigeria: Problems and Prospects. African Journal of International Affairs & Development, 18(1/2), 37-50.

UPI Transactions Reach New Heights With 38% Growth In November. https://english.bharatexpress.com/business/upi-transactions-reach-new-heights-with-38-growth-in-november-181109

Chang, M. (2015). Perceived Factors Influencing the Acceptance and Adoption of Self-service Technology. https://core.ac.uk/download/672498789.pdf

Statista – India Funding in Fintech

Statista. (n.d.). India: Funding in fintech (annual). https://www.statista.com/statistics/1619871/india-funding-in-fintech/

Statista – Neobanking Report

Statista. (n.d.). Neobanking report. https://www.statista.com/study/135798/neobanking-report/

Statista – Number of Neobanking Users in India

Statista. (n.d.). Forecast number of neobanking users in the fintech market in India.

https://www.statista.com/forecasts/1437498/number-of-users-neobanking-fintech-market-india/

Annexure:

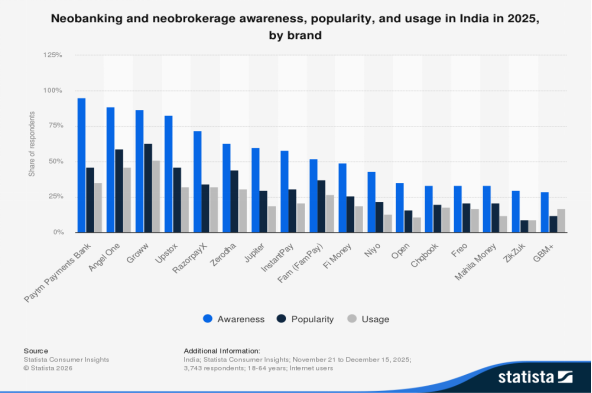

Figure 5: Neobanking and neobrokerage awareness, popularity, and usage in India in 2025, by brand

Source: Statista [https://www.statista.com/statistics/1440720/india-neobank-neobrokerage-popularity-by-brand/ ]

TABLE OF FIGURES

| Figure 1 | Trend Analysis of Global Neo-bank Transaction Value |

| Figure 2 | Trend Analysis of Indian Neo-bank Users |

| Figure 3 | Trend Analysis of Net Profit of Leading Neo Banks in India |

| Figure 4 | Trend Analysis of UPI Transaction Value |

| Figure 5 | Neobanking and neobrokerage awareness, popularity, and usage in India in 2025, by brand |